Financial period closing guide for Missouri businesses

Many Missouri small business owners believe that financial period closing is just about entering the last few transactions before filing taxes. Research shows this misconception affects roughly 70% of small business bookkeepers, leading to preventable errors and compliance issues. Financial period closing is actually a comprehensive process that finalizes, reviews, and locks your books for a specific timeframe, ensuring accuracy and readiness for reporting. This guide explains what financial period closing truly involves, walks you through each step, corrects common myths, and shows Missouri small businesses how to leverage technology and best practices to close your books confidently each period.

Table of Contents

- What Is Financial Period Closing?

- Step-By-Step Financial Period Closing Process

- Common Misconceptions About Financial Period Closing

- Financial Period Closing And Tax Compliance

- Technology And Tools To Streamline Period Closing

- Practical Implications And Case Studies

- Summary And Next Steps For Missouri Small Business Owners

- Start Streamlining Your Bookkeeping Today With Kenworthy Bookkeeping

Key takeaways

| Point | Details |

|---|---|

| Financial period closing locks books for accurate reporting | Proper closing finalizes transactions, reconciles accounts, and prepares reports for each period. |

| Step-by-step process prevents costly errors | Following a consistent closing routine reduces mistakes and streamlines tax compliance. |

| Common misconceptions lead to inaccurate records | Many skip essential reconciliation steps, thinking closing is only transaction entry. |

| Technology tools save time and improve accuracy | QuickBooks Online automates reconciliation and locking, cutting closing time by up to 30%. |

| Regular closing supports confident business decisions | Timely, accurate financial data empowers better planning and tax readiness. |

What is financial period closing?

Financial period closing is an accounting process that finalizes and locks the books for a specific period, ensuring accurate and reportable data. This isn’t just a technicality for large corporations. Small businesses in Missouri need reliable financial records to file taxes correctly, apply for financing, and make informed decisions about growth and spending.

Most businesses close their books on a monthly, quarterly, or yearly schedule. Monthly closings provide the most timely insights into cash flow and profitability, helping you spot issues early. Quarterly closings align with tax payment deadlines for many businesses. Annual closings prepare your records for tax filing and compliance reporting.

Closing your books means you’ve verified every transaction, reconciled bank accounts, corrected errors, and prepared financial statements that accurately reflect your business performance. Once closed, that period’s data is locked to prevent accidental changes that could compromise your records. This process fits naturally into your bookkeeping routine as the final step each month or quarter, transforming raw transaction data into reliable financial intelligence.

Key elements of the financial period closing process include:

- Verifying all transactions are recorded completely and categorized correctly

- Reconciling bank statements, credit cards, and other accounts to match your books

- Making adjusting entries for accruals, deferrals, depreciation, or corrections

- Generating final financial reports like profit and loss statements and balance sheets

- Reviewing results for accuracy and identifying any anomalies or trends

- Locking the period in your bookkeeping system to preserve data integrity

Without proper closing, your financial reports may contain incomplete data, duplicate entries, or unreconciled discrepancies. These errors cascade into tax filing mistakes, missed deductions, and poor business decisions based on faulty information.

Step-by-step financial period closing process

A structured approach to closing your books each period prevents oversights and builds confidence in your financial data. This systematic month-end close includes reconciling accounts, reviewing transactions, adjusting entries, preparing financial statements, and analyzing results. Here’s how Missouri small businesses can implement an effective closing routine.

-

Gather and organize all financial documents. Collect bank statements, credit card statements, receipts, invoices, and any other transaction records for the period. Having everything in one place before you start saves time and ensures nothing gets missed.

-

Record all transactions completely. Enter any outstanding transactions into your bookkeeping system, including sales, expenses, payments received, and bills paid. Double check that every transaction is categorized correctly according to your chart of accounts.

-

Reconcile all accounts thoroughly. Compare your bookkeeping records against bank statements, credit card statements, and loan accounts. Mark each transaction as cleared when it matches the statement. Investigate and resolve any discrepancies immediately.

-

Make necessary adjusting journal entries. Record accrued expenses you owe but haven’t paid yet, deferred revenue, depreciation, and any corrections discovered during reconciliation. These adjustments ensure your reports reflect the true financial position under accrual accounting principles.

-

Generate and review financial reports. Run your profit and loss statement and balance sheet for the period. Review the numbers carefully for unusual items, unexpected changes, or obvious errors that need correction.

-

Analyze results and document insights. Compare current period results to prior periods and budget expectations. Note any significant variances or trends that require management attention or strategy adjustments.

-

Close and lock the period in your software. Once you’re confident everything is accurate, close the period in your bookkeeping system to prevent accidental changes. This preserves the integrity of your historical records.

Following this monthly financial review process consistently transforms closing from a stressful scramble into a manageable routine. The benefits extend beyond clean books to include faster tax preparation, better cash flow visibility, and informed decision-making throughout the year.

Pro Tip: Create a standardized checklist based on these steps and add items specific to your business. Use the same checklist every period to ensure nothing falls through the cracks. Review your bookkeeping checklist for success and refine it as your business evolves. Following proven bookkeeping best practices and reviewing detailed month-end close steps helps you build a closing process that works efficiently for your Missouri business.

Common misconceptions about financial period closing

Many small business owners hold beliefs about period closing that lead to incomplete processes and inaccurate records. Understanding and correcting these misconceptions helps you avoid costly mistakes and build reliable financial systems.

Misconception: Closing just means recording the last transactions. About 70% of small business bookkeepers mistakenly believe closing is just recording transactions, skipping key reconciliation and review essential for accuracy. In reality, closing encompasses thorough review, reconciliation, adjustments, and report generation. Simply entering transactions without verification leaves errors undetected.

Misconception: Reconciliation is optional or can wait. Some business owners skip bank reconciliation during closing, thinking they can catch up later. This approach doubles your error rate and makes problems harder to trace. Unreconciled accounts hide duplicate entries, missed transactions, and fraudulent activity until they become serious issues.

Misconception: Closing only matters at year end. Waiting until December to close your books creates an overwhelming task and eliminates the benefits of timely financial insights. Monthly or quarterly closing catches errors early, supports better cash flow management, and makes tax filing much less stressful.

Misconception: Adjusting entries aren’t necessary for small businesses. Even small operations need adjusting entries to match revenues and expenses to the correct period. Without adjustments for accruals, deferrals, and depreciation, your reports misrepresent profitability and financial position.

Key principles to remember:

- Complete closing requires verification, reconciliation, adjustments, and reporting, not just transaction entry

- Regular reconciliation is mandatory for accurate books and fraud prevention

- Monthly closing provides the most value through timely insights and error detection

- Proper closing follows consistent procedures documented in checklists and workflows

- Professional guidance helps establish compliant, efficient closing practices

Avoiding these common misconceptions about period closing and following proven bookkeeping tips for small businesses ensures your financial records support business success rather than create compliance headaches.

Financial period closing and tax compliance

Proper financial period closing directly impacts your ability to file accurate tax returns and maintain compliance with IRS and Missouri Department of Revenue requirements. The connection between diligent closing practices and tax success cannot be overstated for Missouri small businesses.

When you close your books correctly each period, you ensure all revenues and expenses are captured completely and categorized properly for tax reporting. This accuracy reduces the risk of underpaying taxes, which triggers penalties and interest, or overpaying, which ties up cash unnecessarily. Regular closing also identifies deductible expenses you might otherwise miss at year end.

Accurate, well-maintained books make tax filing straightforward rather than stressful. Your accountant can prepare returns efficiently when financial data is organized and reconciled. You’ll spend less on tax preparation fees and avoid last-minute scrambles to locate missing receipts or explain discrepancies.

Missouri small businesses benefit from period closing in several tax-related ways:

- Complete transaction records support accurate income reporting on federal and state returns

- Proper expense categorization maximizes legitimate deductions and credits

- Reconciled accounts provide documentation to support tax positions if questioned

- Timely closing enables quarterly estimated tax calculations based on actual performance

- Clean books reduce audit risk by demonstrating organized, compliant record keeping

If the IRS or Missouri Department of Revenue selects your business for examination, closed periods with supporting documentation demonstrate professionalism and compliance. Auditors look favorably on businesses that maintain systematic records and can quickly provide requested information.

Beyond compliance, regular closing supports proactive tax planning. Understanding your profitability each quarter allows strategic decisions about equipment purchases, retirement contributions, or other tax-saving moves before year end. This forward-looking approach to taxes reduces surprises and optimizes your tax position.

The role of proper bookkeeping in tax season extends throughout the year. Each monthly or quarterly close builds the foundation for smooth, accurate, and strategic tax filing that protects your Missouri business from penalties while minimizing your tax burden.

Technology and tools to streamline period closing

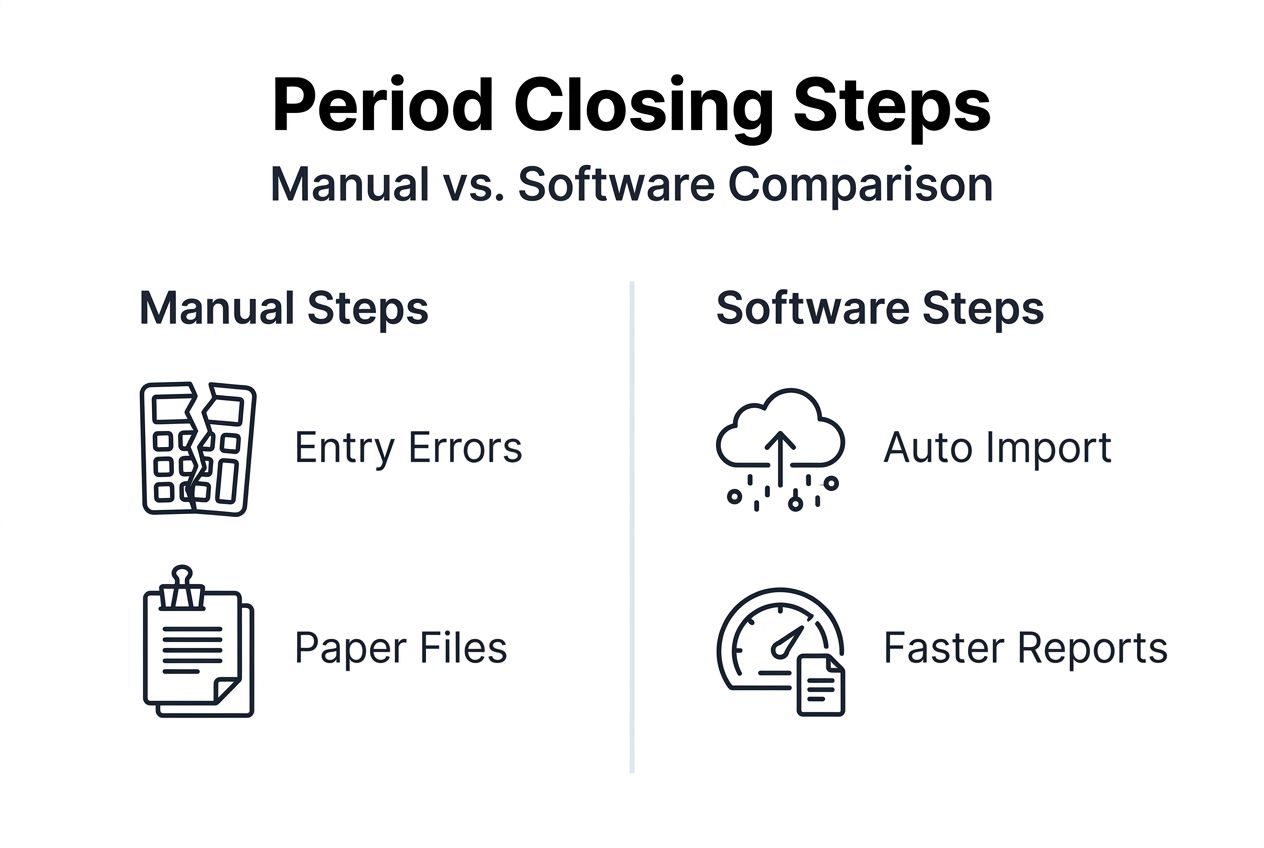

Bookkeeping software transforms period closing from a tedious manual process into an efficient, largely automated routine. Most Missouri small businesses now rely on technology to handle closing tasks faster and more accurately than traditional paper-based methods.

QuickBooks Online stands out as the most popular platform for small business bookkeeping, offering features specifically designed to simplify period closing. QuickBooks Online offers reconciliation and reporting features that simplify period closing for small businesses. The software connects directly to your bank accounts and credit cards, automatically importing transactions and suggesting categorizations based on past patterns.

During reconciliation, QuickBooks Online displays your bookkeeping records alongside bank statement transactions, making it easy to match and clear items. The system flags discrepancies and helps you investigate differences. Once reconciled, you can lock the period to prevent accidental changes to closed months.

Report generation becomes a single-click task in QuickBooks Online. The software maintains real-time profit and loss statements, balance sheets, and cash flow reports based on your transaction data. You can customize reports, compare periods, and export to share with accountants or advisors.

Here’s how manual bookkeeping compares to QuickBooks Online for period closing:

| Aspect | Manual Bookkeeping | QuickBooks Online |

|---|---|---|

| Transaction entry | Hand-written or spreadsheet, time-consuming | Automatic bank feeds, faster entry |

| Reconciliation | Manual comparison, error-prone | Side-by-side matching, flags discrepancies |

| Adjusting entries | Calculated manually, easy to miss | Guided entry, templates for recurring items |

| Report generation | Created from scratch each period | One-click reports, real-time updates |

| Period locking | Discipline-based only, no protection | System-enforced locks preserve data |

| Time required | 8-12 hours per month typical | 3-5 hours per month typical |

| Error rate | 5-10% without double-checking | 1-2% with automated checks |

Automation reduces closing time by up to 30% while significantly cutting errors. Beyond time savings, software provides audit trails, multi-user access with permissions, and cloud backup that protects your records from loss or damage.

The investment in bookkeeping software pays for itself quickly through time savings, error reduction, and improved financial insights. Even very small businesses benefit from the structure and automation modern platforms provide.

Pro Tip: Don’t just buy software and expect magic results. Invest time upfront learning the features through tutorials and guides. Set up your chart of accounts thoughtfully. Establish rules for automatic transaction categorization. Use closing period locks religiously. The combination of good software and disciplined processes delivers the best results.

Explore more bookkeeping tips and tools and review QuickBooks Online period closing features to understand how technology can transform your financial management.

Practical implications and case studies

Real-world examples from Missouri small businesses demonstrate how implementing proper financial period closing practices delivers tangible benefits. These case studies illustrate common challenges and practical solutions that work in everyday business operations.

Missouri small businesses using monthly closing report improved accuracy and tax readiness, as shown by Kenworthy Bookkeeping’s client successes. One Kansas City retail client struggled with cash flow surprises and scrambled tax preparation each April. After implementing monthly closing procedures with QuickBooks Online, they gained clear visibility into monthly profitability, caught billing errors quickly, and reduced tax preparation time by 40%.

Another service-based business in Missouri initially closed books only at year end, creating a stressful tax season rush. They faced repeated requests from their accountant for missing documentation and corrections. Switching to quarterly closing with reconciliation cut their tax preparation costs significantly and eliminated the last-minute chaos.

Common challenges Missouri small businesses face during period closing:

- Limited time and staff to handle bookkeeping tasks consistently

- Lack of training on bookkeeping software features and closing procedures

- Missed bank reconciliations leading to undetected errors and discrepancies

- Inconsistent processes without documented checklists or workflows

- Difficulty distinguishing between essential and optional closing steps

Solutions that drive successful outcomes:

- Scheduling dedicated time each month for closing tasks, treating it as non-negotiable

- Investing in QuickBooks Online training or working with a bookkeeping professional initially

- Using standardized checklists adapted from proven templates and practical checklists

- Setting up automated bank feeds and reconciliation reminders in software

- Starting simple with monthly transaction review and reconciliation, then adding sophistication

Businesses that adopt systematic closing practices report multiple benefits beyond just cleaner books. They make better purchasing and hiring decisions based on accurate profitability data. They negotiate more confidently with lenders when seeking financing. They sleep better knowing their tax obligations are tracked properly throughout the year.

The key insight from these Kenworthy Bookkeeping case studies is that period closing doesn’t require perfection or consume excessive time when you establish the right systems. Even small improvements in consistency and accuracy compound into significant advantages over time.

Summary and next steps for Missouri small business owners

Regular financial period closing represents one of the most valuable practices Missouri small business owners can adopt to improve financial accuracy, tax compliance, and business decision-making. This systematic approach to finalizing your books each month or quarter transforms bookkeeping from a dreaded chore into a strategic advantage.

The essential steps bear repeating: gather all financial documents, record transactions completely, reconcile every account thoroughly, make necessary adjusting entries, generate and review financial reports, and close the period in your system. Following this process consistently prevents the accumulation of errors and provides timely insights into your business performance.

Technology, particularly QuickBooks Online, makes closing faster and more accurate by automating transaction imports, streamlining reconciliation, and generating reports instantly. The investment in bookkeeping software and training pays substantial dividends through time savings and improved data quality.

Key actions for Missouri small business owners:

- Commit to monthly closing as your target, or quarterly at minimum

- Implement a documented closing checklist tailored to your business

- Learn or get help with your bookkeeping software’s closing features

- Track your closing time and error rate to measure improvement

- Seek professional guidance to establish efficient, compliant procedures

Whether you handle bookkeeping internally or work with a professional, understanding the period closing process ensures your business maintains the accurate, compliant records essential for long-term success. The practices outlined in this guide provide a roadmap to transform your bookkeeping from reactive record-keeping into proactive financial management.

Your next step is simple: schedule time this week to either perform your next period close following these guidelines or to arrange a bookkeeping consultation in Missouri that will customize a closing process for your specific business needs. Taking action now prevents future headaches and positions your business for confident growth.

Start streamlining your bookkeeping today with Kenworthy Bookkeeping

Kenworthy Bookkeeping specializes in helping Missouri small businesses master financial period closing and establish bookkeeping systems that support growth. Our team understands the unique challenges Kansas City area businesses face and provides tailored solutions that fit your industry, transaction volume, and growth stage.

We offer comprehensive services including transaction categorization, bank reconciliations, monthly financial reports, and complete period closing procedures using QuickBooks Online. Our clients gain accurate, timely financial data without the stress of managing bookkeeping internally. Whether you need ongoing monthly support or initial setup and training, we customize our approach to your needs.

Access our proven bookkeeping success checklist and explore professional bookkeeping consultation options to discover how expert guidance accelerates your progress. Learn more bookkeeping tips that Missouri business owners use to streamline operations and improve profitability. Schedule your consultation today to transform your bookkeeping from a burden into a competitive advantage.

Frequently asked questions

What is the typical financial period for closing in small businesses?

Most small businesses close their books monthly to maintain timely and accurate financial records. Monthly closing provides the most current insights into cash flow, profitability, and financial position, enabling better business decisions. Some businesses close quarterly, particularly if transaction volume is low, while yearly closing is performed primarily for tax filing and annual reporting purposes.

How often should Missouri small business owners perform financial period closing?

Monthly closing represents the best practice for Missouri small businesses seeking accurate tax preparation and timely financial insights. This frequency allows you to catch errors quickly, manage cash flow proactively, and avoid overwhelming work at tax time. Very small businesses with minimal transactions might manage with quarterly closing, but monthly is strongly recommended. Regular closing prevents the last-minute rushes and stress that come with annual-only closing.

Can I perform financial period closing without bookkeeping software?

Manual period closing using paper records or spreadsheets is possible but tends to be extremely time-consuming and error-prone. You’ll spend significantly more hours reconciling accounts, preparing reports, and tracking down discrepancies. Bookkeeping software like QuickBooks Online automates transaction imports, reconciliation matching, and report generation, dramatically improving accuracy while reducing time investment. Missouri small businesses are encouraged to adopt affordable, user-friendly software to make closing manageable and reliable.

What are the risks of not closing financial periods regularly?

Skipping regular period closing significantly increases your risk of inaccurate financial statements and incorrect tax filings. Errors accumulate and become harder to trace when you wait months to reconcile accounts. You’ll miss critical business insights about profitability and cash flow trends. The lack of organized, closed periods raises red flags during IRS or Missouri Department of Revenue audits, potentially triggering penalties. Poor financial data also leads to bad business decisions about spending, hiring, and growth strategies.