Role of General Ledger: Boosting Small Business Success

Juggling day-to-day operations while trying to keep accurate financial records can feel frustrating for many Kansas City home service business owners. When transactions are scattered between receipts, spreadsheets, and bank statements, spotting profit leaks or planning for taxes becomes a challenge. Learning the fundamentals of a general ledger empowers you to organize income and expenses clearly, cut accounting errors, and lay the groundwork for smarter business decisions.

Table of Contents

- General Ledger Fundamentals And Common Myths

- Key Accounts And Double-Entry Bookkeeping

- How General Ledger Drives Financial Reporting

- Legal Compliance And Audit Readiness

- Common Mistakes In General Ledger Management

Key Takeaways

| Point | Details |

|---|---|

| Understanding the General Ledger | A general ledger is essential for tracking all financial transactions, providing a clear overview of business health. |

| Importance of Double-Entry Bookkeeping | This method ensures accuracy by recording every transaction as both a debit and credit, enhancing financial transparency. |

| Value of Financial Reports | Maintaining a general ledger allows for the generation of key financial reports that inform strategic decisions and highlight business performance. |

| Audit Readiness | Keeping an organized general ledger aids in legal compliance and prepares businesses for audits, demonstrating financial responsibility to stakeholders. |

General ledger fundamentals and common myths

A general ledger is the financial backbone of any small business, serving as a comprehensive record of all monetary transactions. Core accounting system that tracks every financial movement with precision and clarity, the general ledger enables business owners to understand their financial health at a glance.

The fundamental structure of a general ledger involves organizing transactions into specific account categories:

Here’s how the main general ledger account categories differ in purpose and examples:

| Account Category | Main Purpose | Common Examples |

|---|---|---|

| Assets | Track what business owns | Cash, inventory, equipment |

| Liabilities | Record what business owes | Loans, accounts payable |

| Equity | Show owner’s investment | Owner’s capital, retained earnings |

| Income | Measure revenue sources | Sales, interest income |

| Expenses | Monitor business outflows | Rent, utilities, salaries |

- Assets: What the business owns

- Liabilities: What the business owes

- Equity: Owner’s financial investment

- Income: Revenue generated

- Expenses: Money spent on business operations

Contrary to popular misconceptions, a general ledger isn’t just a dusty book of numbers. Financial records management is a dynamic process that provides real-time insights into business performance. Small business owners often mistakenly believe that basic spreadsheets or bank statements can replace a comprehensive general ledger system.

The reality is that a well-maintained general ledger offers multiple critical benefits. It supports accurate financial statement preparation, enables precise tax reporting, helps track business performance trends, and provides a clear financial roadmap for strategic decision-making. Each transaction is meticulously recorded using double-entry bookkeeping, where every financial movement is logged as both a debit and credit to maintain perfect balance.

Pro tip: Invest time in understanding your general ledger or work with a professional bookkeeper to ensure your financial records remain accurate and insightful.

Key accounts and double-entry bookkeeping

Double-entry bookkeeping is a sophisticated accounting method that forms the foundation of modern financial record-keeping for small businesses. Fundamental accounting system that ensures every financial transaction is recorded with precision and balance, this approach provides an unparalleled level of financial transparency and accuracy.

The five primary account categories in double-entry bookkeeping include:

- Assets: Resources owned by the business

- Liabilities: Financial obligations and debts

- Equity: Owner’s financial stake in the business

- Income: Revenue streams and monetary inflows

- Expenses: Costs associated with business operations

Each financial transaction in this system requires two corresponding entries – a debit in one account and an equal credit in another. Accounting balance mechanism that mathematically validates every transaction, this approach helps detect errors and prevents accounting discrepancies. Small business owners benefit from this method by gaining a comprehensive view of their financial landscape, enabling more informed strategic decisions.

The power of double-entry bookkeeping lies in its ability to create a self-checking system. When total debits consistently equal total credits, business owners can trust their financial records’ integrity. This method supports accurate financial statement preparation, provides clear insights into business performance, and ensures compliance with standard accounting practices.

Pro tip: Consider working with a professional bookkeeper who can implement double-entry bookkeeping systematically and help you interpret the financial insights effectively.

How general ledger drives financial reporting

The general ledger serves as the critical financial nerve center for small businesses, transforming raw transaction data into meaningful financial insights. Core financial reporting foundation that meticulously tracks every financial movement, the general ledger enables business owners to generate comprehensive reports that reveal the true financial health of their organization.

Key financial reports generated from the general ledger include:

Below is a summary of key financial reports and the main questions each helps answer:

| Report Type | Primary Business Question Answered |

|---|---|

| Balance Sheet | What is my financial position today? |

| Income Statement | Did the business make a profit? |

| Cash Flow Statement | Where is my cash going? |

| Profit and Loss Report | What are my total profits and losses? |

| Accounts Receivable Aging | Which customers owe me money? |

- Balance Sheet: Snapshot of business assets, liabilities, and equity

- Income Statement: Detailed view of revenues and expenses

- Cash Flow Statement: Analysis of money moving in and out of the business

- Profit and Loss Report: Comprehensive overview of financial performance

- Accounts Receivable Aging Report: Tracking outstanding customer payments

Financial data aggregation mechanism that converts individual transactions into strategic insights, the general ledger provides a systematic approach to financial reporting. Small business owners can leverage these reports to make informed decisions, identify potential financial risks, and develop targeted growth strategies. Each transaction is carefully categorized and recorded, creating a transparent and traceable financial narrative.

The power of the general ledger extends beyond simple record-keeping. It serves as a critical tool for financial analysis, tax preparation, and strategic planning. By maintaining a meticulously organized general ledger, business owners can quickly generate accurate financial statements, comply with accounting standards, and provide stakeholders with a clear picture of the company’s financial performance.

Pro tip: Invest in a robust bookkeeping system that can automate general ledger entries and generate real-time financial reports, saving you time and providing instant business insights.

Legal compliance and audit readiness

Audit readiness represents a critical strategic objective for small businesses, ensuring financial transparency and legal protection. Comprehensive audit preparation involves systematic documentation and rigorous financial record management that demonstrates a commitment to accuracy and accountability.

Key elements of maintaining legal compliance include:

- Accurate Record Keeping: Precise transaction documentation

- Financial Statement Integrity: Ensuring GAAP/IFRS compliance

- Regular Reconciliations: Matching subsidiary ledgers with general ledger

- Transparent Documentation: Maintaining clear supporting evidence

- Consistent Reporting: Standardized financial reporting practices

Financial audit preparation standards require meticulous attention to detail in financial record management. Small business owners must develop a proactive approach to compliance, understanding that audits are not just about proving financial accuracy but also about building trust with stakeholders, potential investors, and regulatory bodies.

An organized general ledger serves as the foundation for legal compliance, providing a clear, traceable financial narrative. By implementing robust bookkeeping practices, businesses can minimize audit risks, reduce potential legal complications, and demonstrate financial responsibility. The goal is to create a comprehensive financial documentation system that can withstand the most thorough external scrutiny.

Pro tip: Develop a systematic document retention strategy that preserves financial records for the recommended legal period, making audit preparation seamless and stress-free.

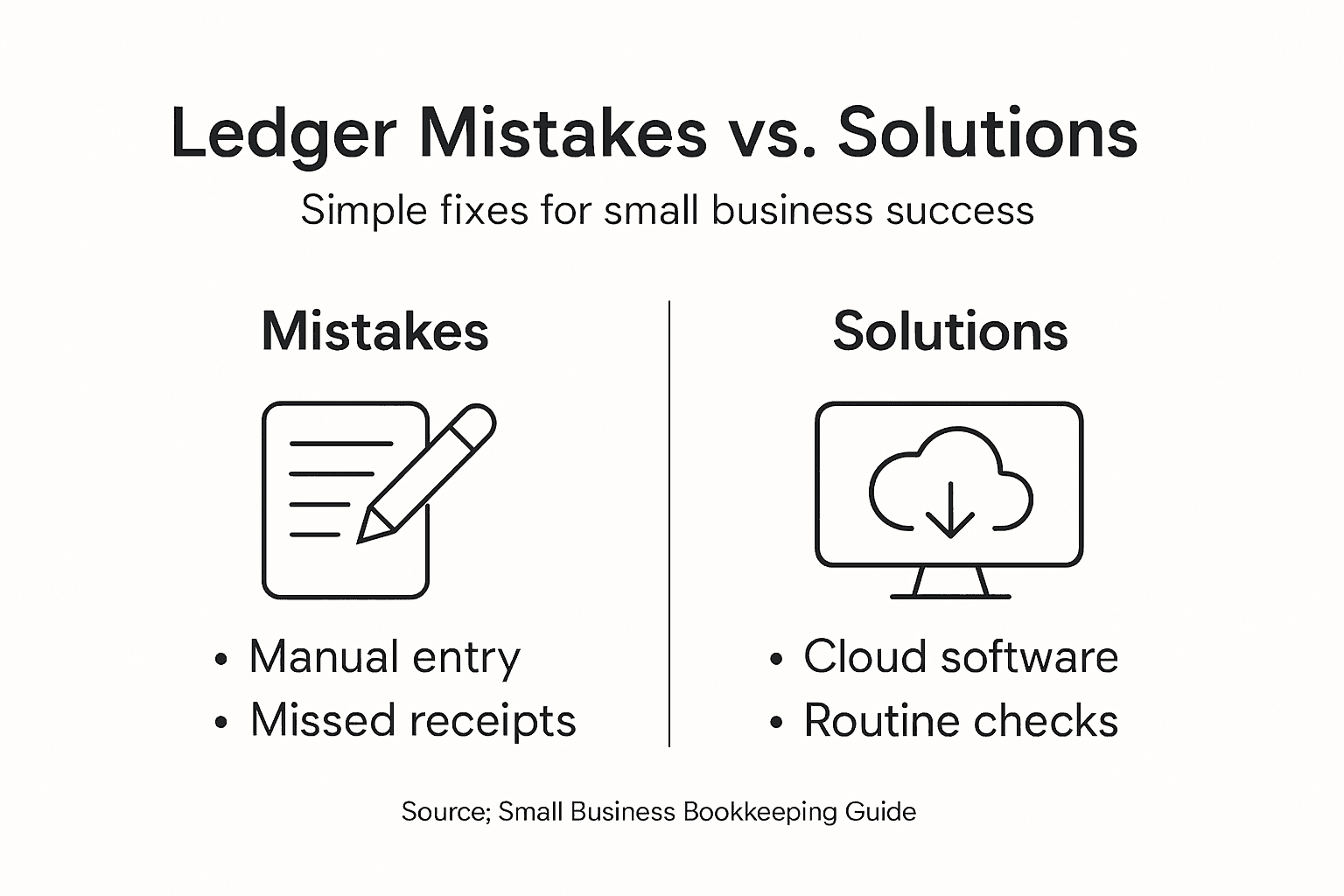

Common mistakes in general ledger management

Managing a general ledger effectively requires precision and consistent attention to detail. Critical bookkeeping error prevention involves understanding the most common pitfalls that can derail financial accuracy and create long-term complications for small businesses.

The most prevalent general ledger management mistakes include:

- Irregular Reconciliation: Failing to match ledger entries with bank statements

- Mixing Personal and Business Finances: Blending transactions across accounts

- Delayed Transaction Posting: Not updating ledger entries timely

- Inadequate Documentation: Poor record-keeping and missing supporting documents

- Inconsistent Accounting Practices: Deviation from standard bookkeeping principles

Financial record management strategies reveal that many errors stem from manual processing and lack of systematic tracking. Small business owners often underestimate the complexity of maintaining accurate financial records, inadvertently creating potential audit risks and financial misrepresentations.

The consequences of these mistakes extend beyond simple bookkeeping errors. Inaccurate ledger management can lead to significant tax complications, missed financial insights, potential legal issues, and reduced credibility with financial institutions. Implementing robust accounting systems, utilizing automated reconciliation tools, and maintaining consistent documentation are crucial steps in mitigating these risks.

Pro tip: Invest in cloud-based accounting software that automatically tracks and categorizes transactions, reducing human error and providing real-time financial insights.

Strengthen Your Small Business with Expert General Ledger Management

Managing a general ledger can feel overwhelming with its demands for accuracy, timely postings, and thorough reconciliations. Kenworthy Bookkeeping understands the challenges of maintaining precise financial records that support double-entry bookkeeping and comprehensive financial reporting. If you want to avoid common pitfalls like delayed transaction entries or mixing personal and business finances, our expert team offers the dedicated support you need to keep your records audit-ready and compliant.

Take control of your business finances today with professional bookkeeping that streamlines your general ledger, bank reconciliations, and tax preparation. Visit Kenworthy Bookkeeping to experience effortless bookkeeping services tailored for small businesses in the Kansas City area. Don’t wait until tax season or an audit—secure your financial clarity now and make informed decisions backed by real-time insights. Explore our comprehensive bookkeeping solutions and see how we simplify financial management so you can focus on growing your business.

Frequently Asked Questions

What is the purpose of a general ledger in small businesses?

A general ledger serves as the financial backbone of a small business, recording all monetary transactions to help owners understand their financial health.

How does double-entry bookkeeping work in relation to the general ledger?

Double-entry bookkeeping requires that every financial transaction is recorded with a corresponding debit and credit entry, ensuring accuracy and balance in financial records.

What key financial reports can be generated from the general ledger?

Key reports include the balance sheet, income statement, cash flow statement, profit and loss report, and accounts receivable aging report. These reports provide insights into financial position, profitability, and cash flow.

What are common mistakes small businesses make in managing their general ledger?

Common mistakes include irregular reconciliation, mixing personal and business finances, delayed posting of transactions, inadequate documentation, and inconsistent accounting practices.

Recommended

- Role of Bookkeeping in Growth for Home Services

- Master Small Business Account Reconciliation Steps Easily

- Role of Bookkeeping for Small Business Success – Kenworthy Bookkeeping Blog

- Business Financial Health Assessment for Small Companies

- Why Track Business Expenses: Financial Control UK – Kefihub

- Revenue Alignment: Scaling B2B Growth With Systems – Kadima