Role of Reconciliation in Bookkeeping Success

Most American small businesses discover hidden errors and even fraud through simple bookkeeping reconciliation. Accurate records matter whether you run a cafe in Texas or a design firm in California. With more than 60 percent of American business owners reporting costly financial mistakes each year, knowing how reconciliation works is crucial. This guide explains the process clearly and shows how choosing the right method helps every business owner keep their finances reliable and secure.

Table of Contents

- Defining Reconciliation In Bookkeeping Processes

- Types Of Reconciliation Used In Small Businesses

- How Reconciliation Works With Quickbooks Online

- Common Pitfalls And How To Avoid Them

- Why Accurate Reconciliation Protects Your Business

Key Takeaways

| Point | Details |

|---|---|

| Importance of Reconciliation | Regular reconciliation is essential for maintaining financial accuracy and detecting errors or fraud. |

| Types of Reconciliation | Small businesses should implement various reconciliation methods such as bank, vendor, and customer reconciliations based on their needs. |

| Using Technology | Leveraging tools like QuickBooks Online can streamline the reconciliation process and enhance financial management efficiency. |

| Proactive Financial Health | Establishing a regular reconciliation schedule not only identifies discrepancies early but also supports overall financial stability and risk management. |

Defining Reconciliation in Bookkeeping Processes

Bookkeeping reconciliation is a systematic process that ensures financial accuracy and integrity. At its core, reconciliation involves comparing transactions and activity to supporting documentation, verifying the validity of financial records and confirming that no unauthorized changes have occurred during processing.

The fundamental goal of reconciliation is matching two distinct sets of financial records to identify discrepancies. Small business owners must understand that this process serves as a critical checkpoint in maintaining accurate financial statements. Reconciliation helps detect potential errors or fraudulent activities by systematically cross-referencing different financial documents and transaction records.

Typical reconciliation processes involve several key steps. Business owners typically compare:

- Bank statements against internal accounting records

- Credit card statements with expense reports

- Accounts payable records with vendor invoices

- Inventory records with physical stock counts

Pro Tip: Monthly Reconciliation Check: Schedule a consistent monthly reconciliation review to catch and resolve financial discrepancies early, preventing potential accounting complications down the line.

Pro Business Strategy: Regular reconciliation transforms your financial tracking from reactive reporting to proactive financial management, giving you real-time insights into your business’s financial health.

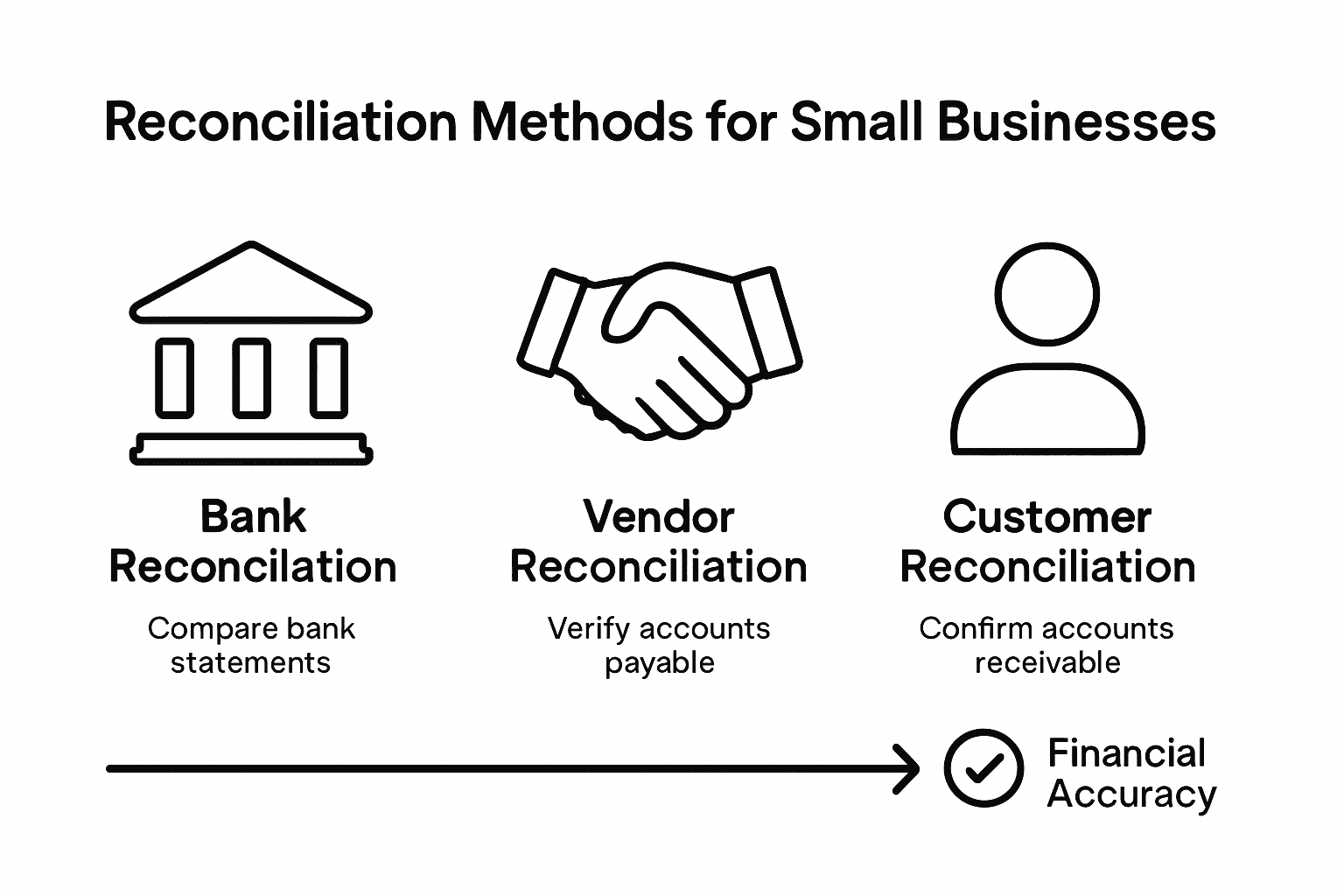

Types of Reconciliation Used in Small Businesses

Small businesses utilize multiple reconciliation methods to maintain financial accuracy and integrity. Small businesses commonly employ various reconciliation types, each designed to address specific financial tracking needs and ensure comprehensive financial management.

The primary types of reconciliation include bank reconciliation, which matches internal financial records with bank statements to identify discrepancies. Vendor reconciliation focuses on aligning accounts payable with vendor statements, ensuring accurate payment tracking and preventing potential billing errors. Customer reconciliation helps verify accounts receivable, guaranteeing that all customer transactions are correctly recorded and accounted for.

Reconciliation methods range from manual to automated approaches, providing businesses flexibility in their financial management strategies:

- Manual Reconciliation: Traditional method involving direct comparison of financial documents

- Spreadsheet Reconciliation: Using software like Excel to track and compare financial records

- Automated Reconciliation: Utilizing specialized accounting software for real-time financial tracking

- Continuous Reconciliation: Ongoing process of regular financial verification and adjustment

Pro Tip: Systematic Reconciliation Strategy: Select a reconciliation method that matches your business complexity, starting with manual processes for smaller operations and gradually transitioning to automated systems as your business grows.

Pro Business Insight: Implementing a consistent reconciliation approach transforms financial record-keeping from a reactive task to a proactive business intelligence tool.

Here’s a comparison of popular reconciliation methods and their ideal business scenarios:

| Method | Best for Business Size | Efficiency Level | Technology Required |

|---|---|---|---|

| Manual Reconciliation | Sole proprietors, startups | Low, time-intensive | None |

| Spreadsheet Reconciliation | Small businesses, early growth | Moderate, improves tracking | Basic spreadsheet software |

| Automated Reconciliation | Growing and established businesses | High, very efficient | Specialized accounting software |

| Continuous Reconciliation | Businesses with frequent transactions | Highest, real-time accuracy | Advanced accounting systems |

How Reconciliation Works With QuickBooks Online

QuickBooks Online provides small businesses with a streamlined approach to financial reconciliation. Reconciliation in QuickBooks Online involves comparing bank, credit card, and loan statements with accounting records to verify the accuracy of every financial transaction and maintain data integrity.

The platform offers a systematic reconciliation process that simplifies complex financial tracking. Users can connect their bank accounts directly to QuickBooks, allowing automatic transaction imports and real-time financial monitoring. This seamless integration enables business owners to match transactions, identify discrepancies, and ensure that every financial record aligns perfectly with bank statements.

Key features of QuickBooks Online reconciliation include:

- Automatic bank feed synchronization

- One-click transaction matching

- Detailed transaction history tracking

- Real-time discrepancy identification

- Comprehensive financial reporting

The reconciliation workflow typically involves several critical steps:

- Connect bank and credit card accounts

- Review imported transactions

- Categorize and match transactions

- Resolve any outstanding differences

- Generate reconciliation reports

Pro Tip: QuickBooks Reconciliation Strategy: Schedule weekly reconciliation reviews to catch and resolve financial discrepancies quickly, preventing potential accounting complications.

Pro Business Insight: Leveraging QuickBooks Online’s reconciliation tools transforms financial management from a time-consuming task to an efficient, strategic business process.

Common Pitfalls and How to Avoid Them

Errors in reconciliation often stem from timing differences, unrecorded transactions, or fraudulent activities, presenting significant challenges for small business owners attempting to maintain accurate financial records. Understanding these common pitfalls is the first step in developing a robust reconciliation strategy that protects your business’s financial integrity.

The most frequent reconciliation mistakes include incomplete transaction tracking, delayed bank statement reviews, and inconsistent record-keeping. Small business owners frequently struggle with manual data entry errors, missed transactions, and failing to reconcile accounts regularly. These oversights can lead to significant financial discrepancies that may go unnoticed for extended periods, potentially causing serious accounting complications.

Key reconciliation pitfalls to watch for include:

- Duplicate Transaction Recording: Accidentally entering the same transaction multiple times

- Overlooked Bank Fees: Missing small bank charges or service fees

- Unreconciled Pending Transactions: Leaving temporary or incomplete transactions unresolved

- Inconsistent Categorization: Misclassifying expenses or income

- Delayed Reconciliation: Waiting too long between reconciliation periods

Preventive strategies to minimize reconciliation errors:

- Implement daily or weekly transaction reviews

- Use automated bank feed synchronization

- Maintain detailed transaction documentation

- Set up transaction matching alerts

- Create a consistent reconciliation schedule

Pro Tip: Error Prevention Protocol: Establish a monthly reconciliation review with a systematic checklist to catch and correct potential discrepancies before they become significant financial issues.

Pro Business Insight: Proactive reconciliation is not just about finding errors, but creating a comprehensive financial management system that provides real-time insights into your business’s financial health.

Why Accurate Reconciliation Protects Your Business

Accurate reconciliation safeguards a business by ensuring financial information’s accuracy and validity, serving as a critical protective mechanism against potential financial risks. Small business owners who implement rigorous reconciliation processes create a robust defense against errors, fraud, and financial mismanagement that could compromise their company’s financial health.

Financial Protection Mechanisms emerge through consistent reconciliation. Regular and precise reconciliation helps uncover bookkeeping errors and potential fraudulent transactions, allowing business owners to make timely adjustments that maintain the integrity of financial records. This proactive approach reduces the likelihood of significant financial discrepancies that could lead to costly audits, tax complications, or legal challenges.

Key protective benefits of accurate reconciliation include:

- Early Fraud Detection: Identifying unauthorized transactions quickly

- Accurate Financial Reporting: Ensuring financial statements reflect true business performance

- Tax Compliance: Maintaining clean, verifiable financial records

- Cash Flow Management: Understanding actual financial position

- Risk Mitigation: Preventing potential financial losses

Strategic approaches to leveraging reconciliation as a protective tool:

- Implement daily transaction reviews

- Use automated reconciliation tools

- Maintain detailed financial documentation

- Create clear audit trails

- Establish multiple verification checkpoints

Pro Tip: Financial Defense Strategy: Treat reconciliation as your business’s financial immune system, conducting regular check-ups to catch and neutralize potential financial threats before they become serious issues.

Pro Business Insight: Accurate reconciliation transforms financial management from a reactive task to a proactive business protection strategy, providing peace of mind and financial security.

Use this table as a quick summary of reconciliation benefits for small businesses:

| Protective Benefit | Description | Business Impact |

|---|---|---|

| Early Fraud Detection | Finds unauthorized activity early | Minimizes financial losses |

| Accurate Reporting | Ensures correct financial statements | Builds stakeholder trust |

| Reliable Tax Compliance | Maintains audit-ready records | Reduces risk of penalties |

| Stronger Cash Flow Insight | Clarifies available funds | Enables better planning |

| Better Risk Management | Identifies and addresses issues | Increases financial stability |

Take Control of Your Bookkeeping with Expert Reconciliation Support

Accurate reconciliation is the backbone of successful bookkeeping. This article highlights common challenges like missing transactions, delayed reviews, and duplicate entries that can put your business at risk. If you want to avoid costly mistakes, detect fraud early, and gain clear insight into your cash flow, you need a proven system that keeps your financial records accurate and up to date.

Kenworthy Bookkeeping specializes in effortless bookkeeping services designed to help small businesses leverage QuickBooks Online for seamless reconciliations. Our expert team ensures your bank statements, credit card records, and internal transaction logs match perfectly every month.

Ready to transform reconciliation from a frustrating task into a powerful business advantage? Visit Kenworthy Bookkeeping Consult and discover how our tailored services in categorization, bank reconciliations, P&L reporting, and tax preparation will put you back in control. Dont wait until discrepancies become problems. Act now and secure your businesss financial health with trusted bookkeeping support.

Frequently Asked Questions

What is the purpose of reconciliation in bookkeeping?

Reconciliation in bookkeeping is the process of comparing financial records to ensure accuracy and integrity. It helps identify discrepancies and detect errors or fraudulent activities by cross-referencing different financial documents.

What types of reconciliation are used in small businesses?

Small businesses commonly utilize bank reconciliation, vendor reconciliation, and customer reconciliation methods to manage their financial records. These methods vary in their focus, from aligning internal records with bank statements to verifying accounts payable and receivable.

How does QuickBooks Online streamline the reconciliation process?

QuickBooks Online simplifies reconciliation by allowing users to connect their bank accounts for automatic transaction imports and real-time financial monitoring. It offers features like transaction matching and discrepancy identification to maintain financial accuracy efficiently.

What are common pitfalls to avoid during reconciliation?

Common pitfalls during reconciliation include duplicate transaction recording, overlooked bank fees, and inconsistent categorization of transactions. To avoid these errors, implement a systematic reconciliation strategy with regular reviews and use automated tools for accuracy.