Master Budget Planning Workflow for Small Businesses

Over half of American small business owners report that financial planning keeps them up at night. Mastering the basics of budgeting, expense tracking, and workflow reviews matters because every missed detail can put your company at risk. This guide breaks down proven steps to help you gain control over your business finances, from assessing your current position to organizing accounts and making smarter budget decisions.

Table of Contents

- Step 1: Assess Current Financial Position

- Step 2: Set Clear Business Goals And Budgets

- Step 3: Organize Accounts In Quickbooks Online

- Step 4: Allocate Funds To Key Expense Categories

- Step 5: Review And Adjust Workflows For Accuracy

Quick Summary

| Key Point | Explanation |

|---|---|

| 1. Assess Your Financial Health | Gather key financial documents to understand your income and expenses for better decision-making. |

| 2. Set SMART Business Goals | Establish specific, measurable goals aligned with your financial strategy to guide budgeting efforts. |

| 3. Organize Financial Accounts | Use QuickBooks Online to categorize and streamline your income and expenses for clearer tracking. |

| 4. Allocate Funds Wisely | Strategically distribute funds across essential and variable expenses while maintaining flexibility for growth. |

| 5. Regularly Review Workflows | Conduct monthly financial reviews to adjust budget based on performance and changing market conditions. |

Step 1: Assess current financial position

Knowing your business’s financial health starts with a clear snapshot of your current financial position. This means gathering and analyzing key financial documents that reveal exactly where your money is coming from and going. By understanding these details, you’ll make smarter decisions that can help stabilize and grow your business.

To begin, collect your most recent financial statements, specifically your balance sheet, income statement, and cash flow report. These documents will help you calculate critical financial ratios that provide insights into your company’s short-term financial stability. Focus on metrics like the current ratio, which shows your ability to cover short-term liabilities with existing assets. A ratio above 1 indicates you can meet your immediate financial obligations.

Pro tip: Don’t just glance at the numbers. Take time to understand what they represent. Look for trends in your revenue, expenses, and cash reserves. Are your expenses consistently higher than income? Are you maintaining enough cash to cover unexpected costs? These insights will guide your budgeting and financial planning strategies. Once you’ve completed this assessment, you’ll be ready to move on to creating a strategic budget that aligns with your business goals.

Step 2: Set clear business goals and budgets

Building a successful budget starts with setting precise business goals that guide your financial strategy. The most effective approach involves creating SMART goals that provide a clear roadmap for your business financial planning. These goals should be specific, measurable, achievable, relevant, and time-bound to ensure you have concrete targets to work toward.

Start by breaking down your goals into short-term and long-term categories. Prioritize strategic expense management by aligning every potential expense with your core business objectives. For each goal, determine the financial resources required and create corresponding budget allocations. This might mean setting aside funds for marketing, equipment upgrades, staff training, or potential expansion opportunities. Track your progress regularly and be prepared to adjust your budget as your business evolves and market conditions change.

Pro tip: Don’t create a budget in isolation. Involve key team members who understand different aspects of your business operations. Their insights can help you identify potential cost-saving opportunities and ensure your budget reflects realistic expectations and growth potential. With a well-crafted budget, you’ll transform financial planning from a mundane task into a strategic tool for business success.

Step 3: Organize accounts in QuickBooks Online

Setting up your financial accounts in QuickBooks Online is a critical step in streamlining your business bookkeeping. The goal is to create a clear, organized system that makes tracking income, expenses, and financial performance simple and intuitive. Proper account organization will save you time and provide accurate insights into your business finances.

Start by creating separate categories for your primary revenue streams and expense types. This might include income accounts like product sales, service revenue, and consulting fees, alongside expense accounts such as utilities, payroll, marketing, and office supplies. Use QuickBooks Online’s chart of accounts feature to customize your financial categories. Group similar transactions together and use consistent naming conventions that make sense for your specific business model. Consider creating subcategories that provide more granular tracking of your financial activities.

Pro tip: Regularly review and reconcile your accounts to ensure accuracy. Set aside time each month to match your QuickBooks entries with bank statements, catching any discrepancies early. This habit will help you maintain clean financial records and quickly identify any potential issues or unexpected expenses. As you become more comfortable with the system, you’ll transform your bookkeeping from a tedious task into a powerful tool for understanding your business’s financial health.

Step 4: Allocate funds to key expense categories

Allocating funds strategically across your business expense categories is crucial for maintaining financial stability and supporting growth. Your budget needs to reflect both your current operational requirements and your future business objectives, creating a financial roadmap that guides smart spending decisions.

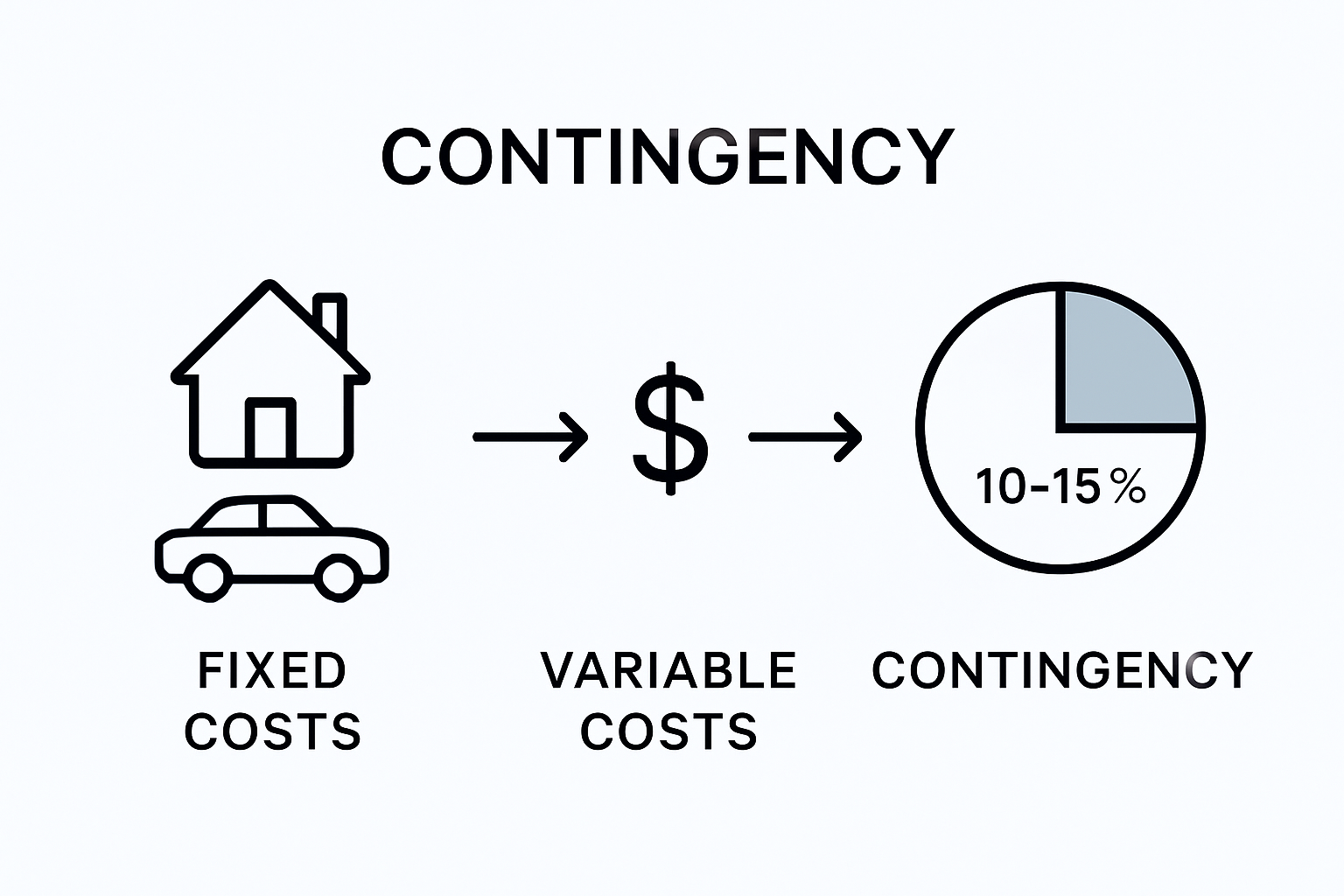

Regular budget examination helps businesses adapt to changing needs by prioritizing essential expenses while maintaining flexibility. Start by categorizing your expenses into fixed and variable costs. Fixed costs might include rent, insurance, and salaries, while variable costs could encompass marketing, supplies, and seasonal inventory. Aim to allocate approximately 50-70% of your budget to essential fixed expenses, leaving room for strategic investments and unexpected opportunities. Prioritize spending that directly contributes to revenue generation or operational efficiency.

Pro tip: Create a contingency fund within your budget allocation that represents 10-15% of your total expenses. This buffer provides financial breathing room during unexpected challenges or potential business growth opportunities. By maintaining this flexible approach to fund allocation, you’ll build financial resilience and position your business to respond quickly to market changes and emerging opportunities.

Step 5: Review and adjust workflows for accuracy

Maintaining accurate financial workflows requires consistent monitoring and strategic adjustments. Your budget is a living document that should evolve alongside your business, reflecting changing market conditions, operational needs, and growth opportunities.

Regular financial reviews are critical for small business success, helping you catch potential issues before they become significant problems. Schedule monthly or quarterly review sessions to analyze your financial performance against initial budgetary goals. Compare actual expenses to projected amounts, identifying areas of overspending or unexpected cost savings. Be strategic about every expense and remain flexible with your budgeting approach, particularly during periods of significant business or market changes.

Pro tip: Create a dedicated financial review team or assign a specific team member to oversee these assessments. This approach ensures consistent accountability and provides a systematic way to track financial performance. By treating your budget as a dynamic tool rather than a static document, you’ll develop a more responsive and resilient financial strategy that supports your business growth and adapts to changing market conditions.

Take Control of Your Budget Planning with Expert Bookkeeping Support

Mastering the budget planning workflow for your small business takes more than just numbers. It requires precision in account organization, strategic fund allocation, and regular financial reviews to keep everything on track. If you are struggling with managing your QuickBooks Online accounts or aligning your budgeting process with your business goals, you are not alone. Many small business owners face challenges such as ensuring expense categorization accuracy and maintaining financial flexibility for unexpected costs.

Kenworthy Bookkeeping specializes in turning these complex financial tasks into effortless processes tailored for small businesses in the Kansas City area. From comprehensive QuickBooks Online account setup and categorization to expert bank reconciliations and detailed P&L reports Kenworthy Bookkeeping helps you streamline your budget management and increase profitability.

Don’t let bookkeeping overwhelm your business growth. Take the next step today by scheduling a personalized consultation at Kenworthy Bookkeeping. Empower your business with clear financial insights and expert guidance to maintain a strategic, adaptable budget that supports your goals and prepares you for any challenge.

Frequently Asked Questions

How can I assess my current financial position?

Understanding your current financial position starts with gathering your financial statements, such as your balance sheet, income statement, and cash flow report. Review these documents to calculate key financial ratios, like the current ratio, which shows your ability to cover short-term liabilities. Analyze these figures to make informed financial decisions and identify areas for improvement.

What are SMART goals in budget planning?

SMART goals are specific, measurable, achievable, relevant, and time-bound targets that guide your financial strategy. For effective budget planning, break your goals down into short-term and long-term categories, ensuring each goal has a clear financial allocation. This structured approach will help you stay focused and assess your progress regularly.

How do I organize my accounts in QuickBooks Online?

To organize your accounts in QuickBooks Online, start by creating categories for your revenue streams and expense types. Use the chart of accounts feature to customize these categories and group similar transactions. Regularly review your accounts to maintain accuracy and simplify your bookkeeping process.

How should I allocate funds across different expense categories?

Allocate funds by categorizing your expenses into fixed and variable costs, ensuring about 50-70% of your budget goes to essential fixed expenses. Create a contingency fund representing 10-15% of your total expenses to cover unexpected costs. Prioritizing your spending will help maintain financial stability and support growth.

Why is it important to review and adjust my budget regularly?

Regularly reviewing and adjusting your budget is crucial for identifying potential overspending and ensuring your financial strategy remains aligned with your business goals. Schedule these reviews monthly or quarterly to analyze actual expenses versus your budget. This practice will help you adapt to changing market conditions and enhance your financial resilience.

Recommended

- Small Business Accounting: Streamlining Your Kansas City Finances – Kenworthy Bookkeeping Blog

- Role of Bookkeeping for Small Business Success – Kenworthy Bookkeeping Blog

- Role of a Bookkeeper: Impact on Kansas City Small Businesses – Kenworthy Bookkeeping Blog

- Kenworthy Bookkeeping Blog

- Master the Construction Cost Breakdown Workflow in the UK – My Project Estimating

- B2B Marketing Strategy Template – Kadima

4 Comments

Comments are closed.