Master the Bank Reconciliation Process for Small Businesses

Nearly half of all American small business owners admit they have struggled with bank reconciliation at least once. Staying on top of your finances is not just about paying bills on time. It is about making sure your records actually match what your bank shows. This step by step guide explains how to properly gather documents, catch errors, and maintain accurate accounting so your American business stays financially healthy.

Table of Contents

- Step 1: Gather Financial Statements and Transaction Records

- Step 2: Review and Categorize All Bank Transactions

- Step 3: Compare Transactions with Accounting Records

- Step 4: Identify and Resolve Discrepancies

- Step 5: Finalize and Save Reconciliation Reports

Quick Summary

| Main Insight | Explanation |

|---|---|

| 1. Gather All Financial Records | Collect your bank statement and internal ledgers to compare and validate transactions accurately during reconciliation. |

| 2. Review Transactions Thoroughly | Analyze each transaction by matching bank entries with internal records to identify discrepancies or errors effectively. |

| 3. Categorize Transactions for Clarity | Organize transactions into clear categories like expenses and income to understand financial patterns and streamline reconciliation. |

| 4. Document and Resolve Discrepancies | Create a comprehensive list of discrepancies, investigate their causes, and update records to ensure accurate financial reporting. |

| 5. Preserve Reconciliation Reports Safely | Generate and securely store reports that summarize findings, ensuring easy retrieval for audits and financial assessments. |

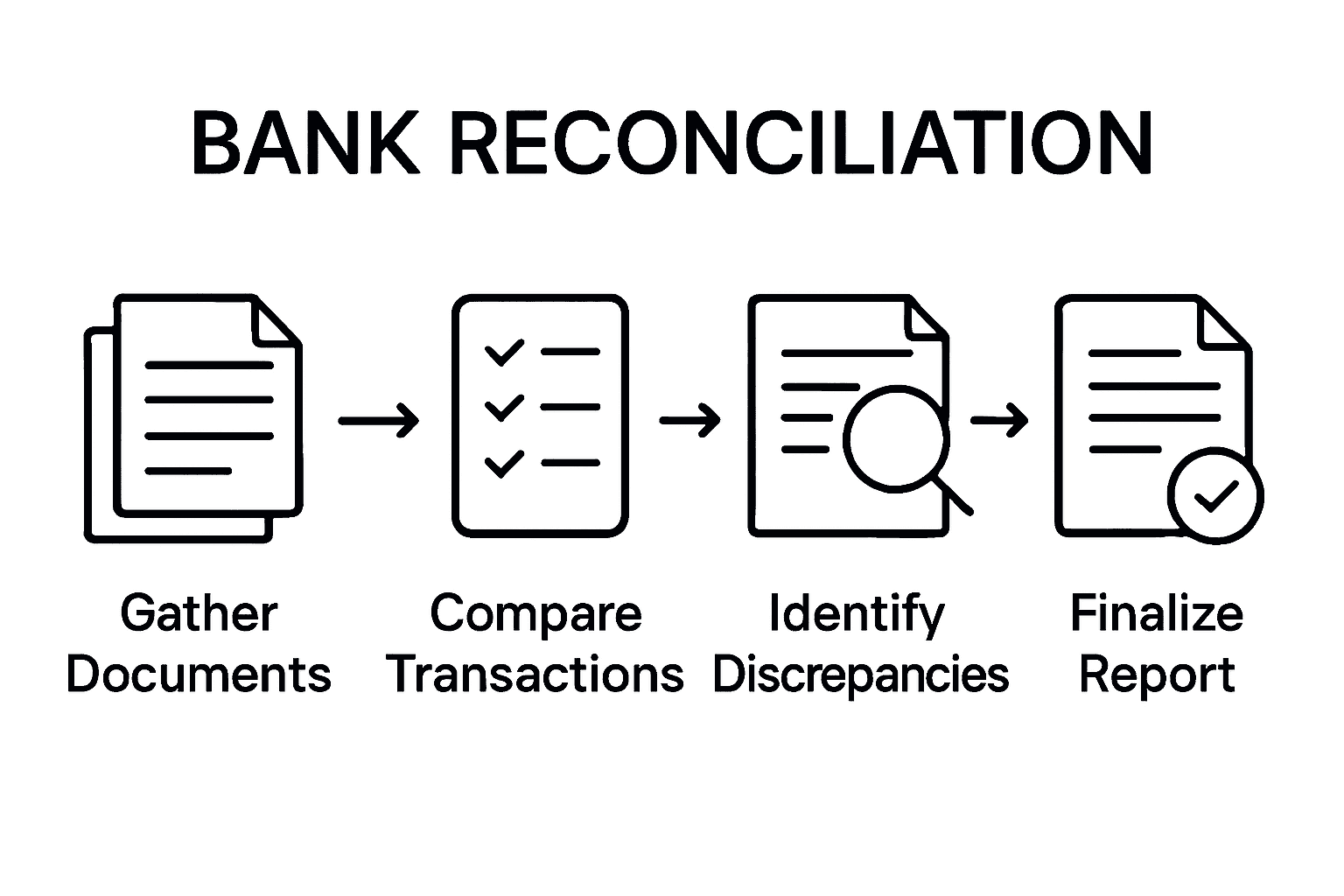

Step 1: Gather Financial Statements and Transaction Records

To kickstart your bank reconciliation process, you’ll need to collect specific financial documents that paint a complete picture of your business’s monetary movements. The goal here is simple: assemble all the necessary paperwork to cross reference and validate your financial transactions accurately.

Begin by pulling together two critical sets of records. First, retrieve your bank statement from your financial institution, which provides an official record of all transactions processed through your business account. Second, collect your internal financial ledger or general transaction records, which tracks the financial activities recorded by your business. These documents will serve as your primary sources for comparing and reconciling discrepancies.

Your collection should include the most recent bank statement covering the period you intend to reconcile, along with corresponding internal financial records such as cash receipts, deposit slips, canceled checks, and accounting journal entries. Organize these documents chronologically to streamline the reconciliation process and make tracking individual transactions easier.

Pro tip: Create a dedicated digital or physical folder for each reconciliation period to keep your financial documents organized and easily accessible for future reference or potential audit requirements.

Step 2: Review and Categorize All Bank Transactions

With your financial documents assembled, the next critical phase of bank reconciliation involves carefully reviewing and categorizing each transaction to ensure accuracy and clarity. This meticulous process helps you understand exactly where your business money is moving and identify any potential discrepancies.

Start by comparing each bank transaction against your internal financial records. Go through every line item methodically, matching bank statement entries with corresponding journal entries in your accounting system. Pay special attention to checks you have issued, verifying which ones have cleared the bank and which might still be outstanding. Look for transactions that might not match exactly income amounts, dates, or descriptions that could signal potential errors or missing information.

As you review, create clear categories for your transactions such as operating expenses, payroll, vendor payments, income streams, and miscellaneous costs. This categorization will not only help during reconciliation but also provide valuable insights into your business financial patterns. Some transactions might require additional investigation if they do not align perfectly between your bank statement and internal records.

Pro tip: Use color coding or digital highlighting in your spreadsheet to quickly identify transactions that require further research or follow up, making your reconciliation process more efficient and organized.

Step 3: Compare Transactions with Accounting Records

In the bank reconciliation process, comparing your bank statement transactions with your internal accounting records is a crucial step that helps you identify potential discrepancies and ensure financial accuracy. This detailed comparison will reveal any differences between what your bank reports and what your business has recorded.

Begin by carefully comparing deposits recorded in your general ledger with those listed on your bank statement. Look for deposits that might be in transit, meaning they have been recorded in your accounting system but not yet reflected in the bank statement. These could include checks you have received but the bank has not yet processed, or electronic payments that are pending. Pay close attention to the dates, amounts, and transaction details, noting any variations that might indicate a recording error or a timing difference.

As you work through each transaction, create a systematic method for tracking and marking discrepancies. Some transactions might appear differently on the bank statement compared to your accounting records due to timing issues, bank fees, interest payments, or unrecorded expenses. Document these differences carefully, as they will be critical in understanding and resolving any inconsistencies in your financial records.

Pro tip: Create a separate worksheet or column in your reconciliation document specifically for noting and explaining any discrepancies, which will help you track and resolve financial inconsistencies more efficiently.

Step 4: Identify and Resolve Discrepancies

Resolving discrepancies is the most critical phase of bank reconciliation where you carefully investigate and address any differences between your bank statement and accounting records. This step requires a methodical approach to ensure your financial records remain accurate and transparent.

Note and analyze discrepancies between your bank statement balance and accounting records, paying close attention to factors like deposits in transit, outstanding checks, interest payments, and unexpected bank fees. Start by creating a comprehensive list of all variations, categorizing them based on their potential origin. Some common discrepancies might include unrecorded bank transactions, timing differences in check deposits or payments, automatic bank service charges, or interest income that has not been previously logged in your accounting system.

For each identified discrepancy, investigate the root cause and determine the appropriate adjustment. This might involve contacting your bank for clarification on specific charges, reviewing your internal record keeping processes, or updating your accounting entries to reflect the actual transaction details. Some discrepancies may require additional documentation or communication with your financial institution to fully resolve. Remember that small differences can accumulate over time, potentially leading to significant accounting errors if left unaddressed.

Here’s a quick reference to common types of reconciliation discrepancies and how to address them:

| Discrepancy Type | Possible Cause | Resolution Method |

|---|---|---|

| Deposits in Transit | Deposit recorded but not yet in bank | Wait for bank to process deposit |

| Outstanding Checks | Issued checks not cleared | Track bank clearing dates |

| Unrecorded Bank Fees | Service charges by bank | Enter fee into accounting records |

| Interest Income | Bank pays interest not yet recorded | Add to accounting income |

| Data Entry Errors | Typos or wrong amounts entered | Correct the entries as needed |

Pro tip: Develop a standardized tracking system for discrepancies that includes columns for the date, description, amount, and resolution status, which will help you maintain a clear audit trail and quickly identify recurring issues.

Step 5: Finalize and Save Reconciliation Reports

As you complete your bank reconciliation process, the final step involves carefully documenting and preserving your financial analysis. This crucial stage transforms your detailed investigation into an official record that protects your business and provides a clear snapshot of your financial health.

Generate a comprehensive bank reconciliation statement that summarizes all bank account transactions and internally recorded transactions. Verify that the adjusted bank balance and your accounting records balance precisely match. Include a detailed breakdown of all reconciliation adjustments, noting specific dates, transaction types, and reasons for any discrepancies you discovered during the process. This documentation serves as an important audit trail and helps you track your business financial accuracy over time.

Ensure your reconciliation report includes key elements such as the starting bank statement balance, total deposits, total withdrawals, bank fees, interest income, and the final reconciled balance. Double check all calculations and create a clean, organized document that clearly shows how you arrived at the final balanced figure. Store these reports securely both digitally and in physical form, maintaining a consistent filing system that allows for easy retrieval during tax preparation or potential financial reviews.

This summary highlights the essential elements for an effective reconciliation report:

| Report Element | Purpose | Why It’s Important |

|---|---|---|

| Starting Bank Balance | Shows opening funds | Establishes point of reference |

| Total Deposits | Sums all deposits for the period | Tracks incoming funds |

| Total Withdrawals | Sums all outflows | Tracks outgoing payments |

| Bank Fees and Charges | Lists fees and deductions | Identifies cost impacts |

| Interest Earned | Records interest received | Reflects additional income |

| Final Reconciled Balance | Confirmed matching totals | Ensures complete accuracy |

Pro tip: Create a digital and physical backup of your reconciliation reports, storing them in both a secure cloud storage system and a fireproof filing cabinet to protect against potential data loss or unexpected disasters.

Simplify Your Bank Reconciliation with Expert Bookkeeping Support

Mastering the bank reconciliation process can be a complex and time-consuming challenge for many small businesses. From gathering detailed financial documents to identifying and resolving discrepancies, it demands accuracy, patience, and clear organization. If you find yourself overwhelmed by matching deposits in transit, outstanding checks, or unrecorded bank fees, you are not alone. These pain points often cause stress and can lead to costly errors or missed opportunities to improve your financial health.

At Kenworthy Bookkeeping, we understand the importance of precise bank reconciliations as a foundation for your business’s financial success. Our expert team specializes in providing effortless bookkeeping services tailored to small businesses using QuickBooks Online. We help you with meticulous transaction categorization, timely bank reconciliations, and insightful reports that give you complete control and confidence in your finances. Don’t let reconciliation discrepancies or confusing financial statements hold your business back. Find peace of mind today by exploring how our trusted services can streamline your bookkeeping and help increase your profitability.

Take the next step toward financial clarity and accuracy. Visit our consultation page to schedule your personalized session. Discover how Kenworthy Bookkeeping can relieve the burden of bank reconciliation and set your small business on a clear path to success. Act now and regain control of your business finances with expert support you can trust.

Frequently Asked Questions

What are the essential documents needed for bank reconciliation?

To effectively conduct bank reconciliation, gather your bank statement and your internal financial ledger or transaction records. Ensure you have recent statements and corresponding internal documents organized chronologically to streamline the comparison and resolve discrepancies.

How do I categorize bank transactions during the reconciliation process?

You should review each bank transaction and match it to your internal records, creating categories such as operating expenses, payroll, and income streams. Start by systematically comparing line items to ensure accuracy and identify any transactions that require further investigation.

What steps should I take to resolve discrepancies in bank reconciliation?

Begin by noting any differences between your bank statement and accounting records, categorizing discrepancies based on their causes. Investigate each discrepancy’s root cause and make the necessary adjustments, such as contacting your bank for clarification or updating your internal records.

How can I ensure my reconciliation reports are accurate?

To verify the accuracy of your reconciliation reports, double-check all calculations and ensure that your adjusted bank balance matches your accounting records precisely. Prepare a comprehensive summary that includes all bank transactions, adjustments made, and a clear final reconciled balance, ensuring you have documentation for future reference.

What is the best way to organize my financial documents for future reconciliations?

Create a dedicated digital or physical folder for each reconciliation period to keep all relevant financial documents organized and easily accessible. Maintain a consistent naming convention, and back up documents in both physical and digital formats for easy retrieval during audits or financial reviews.

Recommended

- 7 Key Steps for a Small Business Financial Health Checklist

- Business Financial Statements Guide for Small Businesses – Kenworthy Bookkeeping Blog

- Role of Bookkeeping for Small Business Success – Kenworthy Bookkeeping Blog

- Master Budget Planning Workflow for Small Businesses – Kenworthy Bookkeeping Blog