Why Maintain Financial Records for Small Businesses

Most American home service business owners in Kansas City underestimate the true power of organized financial records. Nearly one out of every three small businesses faces surprise tax issues or missed profits due to incomplete or disorganized paperwork. For business owners juggling customer calls and daily work, clarity around financial documentation makes the difference between lasting success and costly mistakes. This quick guide helps you spot common misconceptions and gives you practical strategies to strengthen your records for greater profitability and tax peace of mind.

Table of Contents

- Defining Financial Records And Common Misconceptions

- Types Of Financial Records Small Businesses Need

- How Organized Records Streamline Tax Preparation

- Legal Requirements For Recordkeeping In Kansas City

- Preventing Financial Mistakes And IRS Penalties

- Maximizing Profitability Through Informed Decisions

Key Takeaways

| Point | Details |

|---|---|

| The Importance of Financial Records | Financial records go beyond mere documentation; they provide critical insights for informed decision-making and financial strategy. |

| Common Misconceptions | Many small business owners mistakenly believe detailed records are only for large companies; all businesses benefit from meticulous record-keeping. |

| Digital versus Traditional Methods | Digital recordkeeping offers advantages in accessibility, organization, security, and cost-effectiveness compared to traditional paper records. |

| Legal Compliance and Risk Management | Proper financial documentation is essential for meeting legal requirements and avoiding costly IRS penalties related to recordkeeping mistakes. |

Defining Financial Records and Common Misconceptions

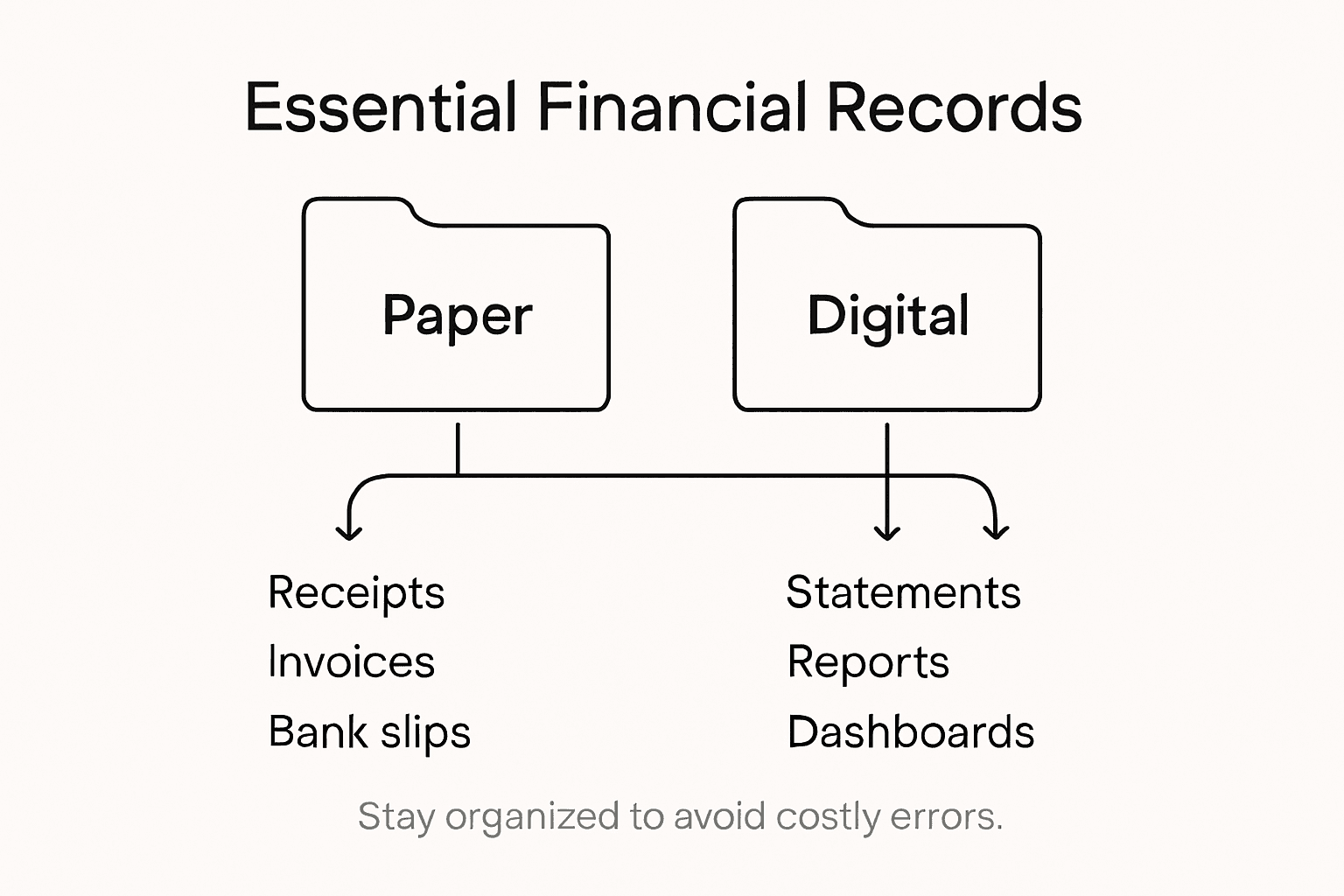

Financial records represent a comprehensive collection of documents tracking a business’s monetary transactions, performance, and fiscal health. From sales receipts and expense reports to tax documents and bank statements, these records form the backbone of understanding a small business’s financial landscape. Critical financial documentation goes far beyond simple number tracking.

Contrary to popular belief, financial records are not just bureaucratic paperwork or tax preparation tools. They serve as strategic roadmaps for business owners, providing critical insights into cash flow, profitability, and potential growth opportunities. Business financial documentation helps entrepreneurs make informed decisions, understand spending patterns, and identify potential areas for cost reduction.

Small business owners often harbor several misconceptions about financial record maintenance. Some believe detailed record-keeping is only necessary for large corporations or during tax season. In reality, consistent and thorough documentation is crucial for businesses of all sizes. These records protect against potential audits, help secure financing, and provide a clear picture of business performance.

Pro Tip – Record Management: Implement a digital filing system that automatically categorizes and stores financial documents, reducing manual work and minimizing the risk of losing critical paperwork.

Here’s a comparison of traditional versus digital financial recordkeeping methods for small businesses:

| Aspect | Traditional Paper Records | Digital Recordkeeping |

|---|---|---|

| Accessibility | Restricted to office location | Accessible from any device |

| Organization | Manual filing, easy misplacement | Automated categorization, searchable |

| Security | Prone to loss, fire, or theft | Data encryption, cloud backups |

| Audit Readiness | Time-consuming to gather | Quick retrieval, easy sharing |

| Ongoing Costs | Printing, storage supplies | Software subscription or cloud fees |

Types of Financial Records Small Businesses Need

Small businesses must maintain a comprehensive set of financial records that provide insights into their fiscal health and support critical business decisions. Essential business financial documentation typically includes several key categories of records that track every financial aspect of the business operations.

These critical financial records encompass multiple document types that serve different strategic purposes. The primary categories include:

- Income Records: Sales receipts, invoices, deposit slips, and payment documentation

- Expense Records: Receipts for business purchases, vendor invoices, credit card statements

- Asset Documentation: Equipment purchases, property records, depreciation tracking

- Tax Documentation: Payroll records, employment tax filings, quarterly and annual tax returns

- Banking Documents: Bank statements, canceled checks, electronic transaction logs

Accurate financial statement tracking requires maintaining comprehensive documentation that allows business owners to understand their financial performance. These documents help create essential financial statements like balance sheets, income statements, and cash flow reports, which provide critical insights into business profitability and financial trends.

Pro Tip – Digital Record Management: Invest in cloud-based accounting software that automatically categorizes and stores financial documents, ensuring secure backup and easy retrieval of important financial records.

How Organized Records Streamline Tax Preparation

Tax preparation can be a daunting process for small business owners, but maintaining well-organized financial records transforms this challenging annual task into a manageable, stress-free experience. Efficient tax documentation serves as the foundation for accurate tax reporting, helping businesses maximize deductions and minimize potential audit risks.

The strategic organization of financial records provides multiple advantages during tax preparation. By systematically categorizing and storing documents throughout the year, small businesses can:

-

Quickly locate specific financial transactions

-

Validate income and expense claims

-

Reduce time spent searching for documentation

-

Ensure accurate reporting of business income

-

Substantiate potential tax deductions

Comprehensive financial record management eliminates last-minute scrambling and reduces the likelihood of errors that could trigger audits or penalties. Businesses with meticulous record-keeping practices can streamline their tax filing process, potentially saving significant time and reducing professional tax preparation costs.

Pro Tip – Systematic Documentation: Create a digital filing system with monthly folders and consistent naming conventions for financial documents, ensuring quick retrieval and organized tax preparation.

Legal Requirements for Recordkeeping in Kansas City

Small businesses in Kansas City must navigate a complex landscape of federal and local recordkeeping regulations that dictate how financial information should be documented, stored, and maintained. Federal recordkeeping guidelines establish baseline requirements for businesses, mandating comprehensive documentation of income, expenses, assets, and tax-related transactions.

The specific legal requirements for Kansas City businesses encompass multiple critical areas:

- Tax Documentation: Maintaining records supporting income and expense claims

- Employment Records: Tracking payroll, employee compensation, and tax withholdings

- Financial Statements: Preserving balance sheets, income statements, and cash flow reports

- Transaction Documentation: Retaining receipts, invoices, and bank statements

- Business Entity Records: Storing incorporation documents and licenses

Small business regulatory compliance requires understanding both Missouri state regulations and federal mandates. Most businesses must retain financial records for a minimum of three to seven years, depending on the specific document type and potential audit requirements. Failure to maintain proper documentation can result in significant penalties, including potential tax assessments and legal complications.

Pro Tip – Record Retention Strategy: Develop a digital and physical document retention system that automatically archives and categorizes financial records, ensuring compliance and easy access during audits or financial reviews.

Preventing Financial Mistakes and IRS Penalties

Small businesses face significant financial risks when they neglect proper recordkeeping and financial management practices. Common financial pitfalls can lead to costly IRS penalties, potentially jeopardizing the entire business operation. The most critical mistakes often stem from poor financial organization and lack of systematic documentation.

Key financial mistakes that can trigger IRS scrutiny include:

- Commingling Funds: Mixing personal and business finances

- Incomplete Expense Tracking: Failing to document all business expenses

- Inconsistent Record Management: Irregular or incomplete financial documentation

- Poor Accounting Practices: Inadequate separation of income and expenses

- Missed Tax Deadlines: Late or incomplete tax filings

Proactive financial compliance is the most effective strategy for avoiding potential penalties. The IRS imposes significant fines for documentation errors, which can range from 20% to 75% of the unpaid tax amount. These penalties can quickly escalate, turning a minor bookkeeping oversight into a substantial financial burden for small business owners.

Pro Tip – Penalty Prevention: Implement a monthly financial review process that cross-checks all transactions, reconciles accounts, and ensures complete documentation to minimize the risk of IRS penalties.

This table summarizes key IRS penalties small businesses could face for poor financial documentation:

| Mistake Type | Potential IRS Penalty | Business Impact |

|---|---|---|

| Incomplete records | Up to 75% of unpaid tax | Severe fines and cash flow issues |

| Missed tax deadlines | Late filing and payment penalties | Damage to financial standing |

| Commingling funds | Disallowance of deductions | Personal assets at increased risk |

| Poor expense tracking | Loss of legitimate deductions | Higher tax liability |

| Inconsistent reporting | Audit or criminal investigation | Legal fees and business disruption |

Maximizing Profitability Through Informed Decisions

Financial records are far more than administrative paperwork. Strategic financial insights transform raw numbers into powerful decision-making tools that can dramatically improve a small business’s bottom line. By systematically tracking and analyzing financial data, entrepreneurs gain unprecedented visibility into their business’s performance and potential growth opportunities.

The most critical financial metrics small businesses should consistently monitor include:

- Revenue Streams: Identifying most profitable services or products

- Expense Patterns: Understanding and controlling cost structures

- Profit Margins: Calculating actual returns on different business activities

- Cash Flow Trends: Predicting potential financial challenges

- Customer Acquisition Costs: Measuring marketing and sales effectiveness

Comprehensive financial analysis enables business owners to make data-driven decisions that go beyond gut feelings. By understanding detailed financial performance, entrepreneurs can strategically allocate resources, cut unnecessary expenses, invest in high-performing areas, and develop targeted growth strategies that maximize profitability.

Pro Tip – Performance Tracking: Create a monthly financial dashboard that visually represents key performance indicators, allowing quick identification of business strengths and potential improvement areas.

Streamline Your Financial Records and Protect Your Small Business Today

Maintaining organized financial records is essential but can quickly become overwhelming. The article highlights key challenges like preventing IRS penalties, ensuring audit readiness, and gaining real insights into profitability. If poor financial documentation and missed deadlines cause you stress or confusion, you are not alone. Our expert bookkeeping team understands these pain points and can help you establish reliable, accurate recordkeeping that meets legal requirements and simplifies tax preparation.

Take control of your business finances with Kenworthy Bookkeeping. Using QuickBooks Online, we offer effortless categorization, bank reconciliations, and comprehensive profit and loss reporting. Don’t wait for costly mistakes or frustrating tax season surprises. Visit Kenworthy Bookkeeping now and schedule a consultation to protect your business and maximize your profitability through trusted financial management.

Frequently Asked Questions

Why are financial records important for small businesses?

Financial records are essential for small businesses because they provide insights into cash flow, profitability, and growth opportunities. They serve as a tool for informed decision-making, aid in securing financing, and protect against audits.

What types of financial records should a small business maintain?

Small businesses should maintain various types of financial records, including income records (sales receipts, invoices), expense records (receipts, vendor invoices), asset documentation (equipment purchases), tax documentation (payroll records), and banking documents (bank statements).

How can organized financial records simplify tax preparation?

Organized financial records streamline tax preparation by allowing quick access to specific transactions, ensuring accurate reporting, validating claims, and reducing time spent searching for documents. This organization minimizes potential audit risks and saves time during tax filing.

What are the common misconceptions about financial record maintenance for small businesses?

Common misconceptions include the belief that only large corporations need detailed record-keeping or that thorough documentation is only necessary during tax season. In reality, consistent record maintenance is critical for small businesses of all sizes to ensure compliance and stability.