Why Small Businesses Need Bookkeeping Services

Managing a small home service business in Kansas City can feel overwhelming when every dollar counts. Accurate bookkeeping gives owners the clarity they need to track income and expenses, avoid costly mistakes, and make wise financial decisions. Whether you handle your books daily or prefer the guidance of a professional, this article explains key concepts and practical methods that strengthen cash flow and simplify business management.

Table of Contents

- Bookkeeping Defined For Small Businesses

- Types Of Bookkeeping Methods Explained

- How Proper Bookkeeping Streamlines Finance

- Legal Requirements And Tax Preparation Needs

- Risks Of Poor Or Neglected Bookkeeping

Key Takeaways

| Point | Details |

|---|---|

| Importance of Bookkeeping | Bookkeeping is essential for small businesses, acting as a financial roadmap for decision-making and growth. |

| Approaches to Bookkeeping | Small businesses can choose between single-entry and double-entry bookkeeping, with double-entry offering enhanced accuracy and insights. |

| Legal Compliance | Accurate record-keeping is vital for tax preparation and compliance with legal obligations, helping avoid penalties and audits. |

| Risks of Poor Practices | Neglecting bookkeeping can lead to financial mismanagement, tax issues, and impaired business operations. |

Bookkeeping Defined for Small Businesses

Bookkeeping is the systematic financial record-keeping process that transforms complex business transactions into clear, manageable financial insights. At its core, bookkeeping involves tracking every financial movement within a business, creating a comprehensive financial narrative that guides strategic decision-making.

Understanding bookkeeping starts with recognizing its fundamental purpose: accurately recording financial transactions. The process acts like a business’s financial GPS, helping owners navigate their monetary landscape by documenting income, expenses, and critical financial patterns.

Key components of bookkeeping for small businesses include:

- Recording daily financial transactions

- Categorizing expenses and income

- Maintaining organized financial records

- Tracking accounts receivable and payable

- Generating financial statements and reports

Small businesses benefit from bookkeeping in multiple strategic ways. It provides clarity on cash flow, helps with tax preparation, enables precise financial forecasting, and offers insights into business performance. By maintaining meticulous financial records, business owners can make informed decisions about growth, investment, and resource allocation.

Pro tip: Start tracking every financial transaction, no matter how small, to build a comprehensive and accurate financial picture of your business.

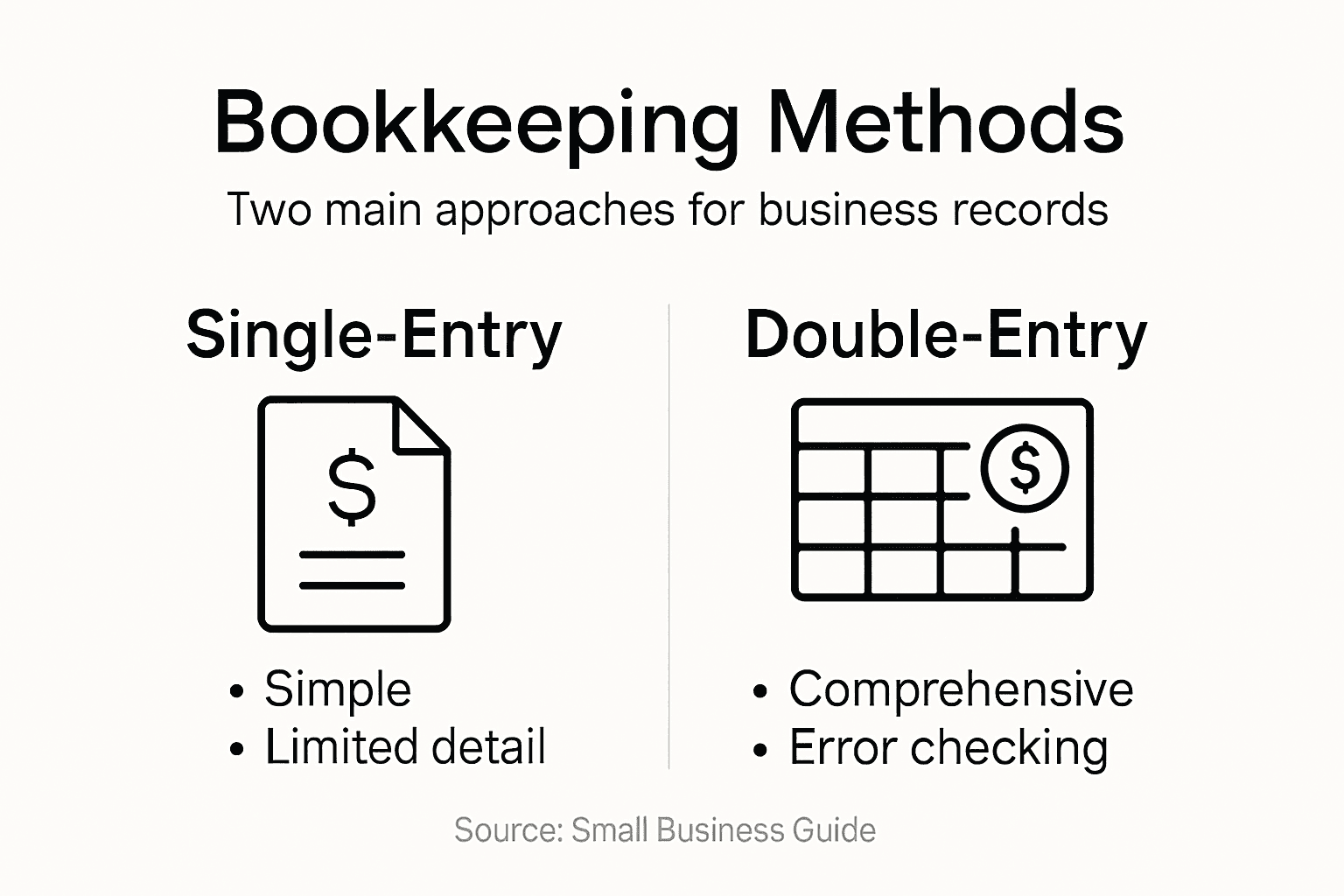

Types of Bookkeeping Methods Explained

Businesses have several approaches to financial record-keeping, with two primary bookkeeping systems dominating the accounting landscape. Understanding these methods is crucial for selecting the most appropriate approach for your small business’s financial management.

Single-entry bookkeeping represents the most basic method of financial tracking. This system involves recording each financial transaction only once, typically in a simple spreadsheet or ledger. Small businesses with minimal transactions often find this method straightforward and less time-consuming.

Key characteristics of single-entry bookkeeping include:

- Tracking income and expenses in a single column

- Minimal complexity in financial recording

- Suitable for very small or service-based businesses

- Lower cost and easier to maintain

- Limited ability to track financial details

Double-entry bookkeeping offers a more sophisticated approach to financial record-keeping. In this system, every transaction is recorded twice – as a debit in one account and a credit in another. This method provides a more comprehensive and accurate representation of a business’s financial health.

Advantages of double-entry bookkeeping encompass:

- Enhanced accuracy in financial reporting

- Ability to detect errors through balanced accounting

- More detailed financial insights

- Better preparation for tax reporting

- Comprehensive tracking of financial movements

Double-entry bookkeeping creates a complete financial picture, allowing business owners to understand their financial position with greater clarity and precision.

Pro tip: Consider consulting a professional bookkeeper to determine which bookkeeping method best suits your specific business needs and complexity.

Here’s how single-entry and double-entry bookkeeping compare for small businesses:

| Feature | Single-Entry Bookkeeping | Double-Entry Bookkeeping |

|---|---|---|

| Record Complexity | Simple transaction list | Records each entry twice |

| Error Detection | Errors often go unnoticed | Easier to spot discrepancies |

| Financial Detail Level | Basic overview | Detailed financial insights |

| Audit and Tax Readiness | Limited preparedness | Strong audit and tax records |

| Suitability | Micro or simple businesses | Growing or complex businesses |

How Proper Bookkeeping Streamlines Finance

Proper bookkeeping is the financial backbone that transforms chaotic business transactions into a clear, strategic roadmap for success. Accurate financial record-keeping enables small businesses to gain unprecedented insights into their financial health, making informed decisions that drive growth and sustainability.

The primary advantage of streamlined bookkeeping lies in its ability to provide real-time visibility into a business’s financial landscape. Financial tracking goes beyond simple number recording – it becomes a powerful tool for understanding cash flow, identifying potential challenges, and uncovering opportunities for strategic investment.

Key benefits of comprehensive bookkeeping include:

- Precise tracking of income and expenses

- Real-time financial performance monitoring

- Enhanced budgeting and financial planning

- Simplified tax preparation

- Improved decision-making capabilities

- Better understanding of business profitability

Small businesses particularly benefit from systematic financial management. By maintaining organized and accurate records, entrepreneurs can:

- Predict cash flow challenges before they become critical

- Identify unnecessary expenses

- Make data-driven investment decisions

- Maintain compliance with tax regulations

- Prepare comprehensive financial reports

Effective bookkeeping transforms financial data from a confusing maze into a clear, actionable roadmap for business success.

Pro tip: Invest in consistent, daily bookkeeping practices to maintain an up-to-the-minute understanding of your business’s financial health.

These bookkeeping practices directly strengthen your business’s financial management:

| Practice | Positive Outcome | Business Impact |

|---|---|---|

| Daily transaction entry | Accurate cash flow monitoring | Enables proactive business changes |

| Organized records | Easier financial analysis | Faster, informed decision-making |

| Regular reviews | Early error detection | Minimizes costly mistakes |

| Digital document storage | Quick compliance verification | Reduces legal and audit stress |

Legal Requirements and Tax Preparation Needs

Small businesses face complex legal obligations when it comes to financial record-keeping and tax compliance. Federal tax recordkeeping guidelines mandate precise documentation of all financial transactions, creating a critical framework for maintaining legal and financial integrity.

Tax documentation represents more than just a bureaucratic requirement – it’s a fundamental aspect of responsible business management. Business owners must maintain comprehensive records that not only satisfy government regulations but also provide strategic insights into their financial operations.

Key legal recordkeeping requirements include:

- Documenting all income sources

- Tracking business expenses with receipts

- Maintaining payroll records

- Preserving financial statements

- Retaining tax returns and supporting documentation

- Recording asset purchases and depreciation

The Internal Revenue Service (IRS) has specific guidelines for small businesses regarding record retention and documentation. These requirements vary depending on business structure, industry, and specific financial circumstances. Businesses must typically maintain financial records for a minimum of three to seven years, ensuring they can substantiate income, deductions, and credits if audited.

Accurate and organized bookkeeping is not just a legal necessity, but a strategic tool for financial management and business growth.

Tax preparation becomes significantly smoother when businesses maintain consistent, detailed financial records. By implementing systematic bookkeeping practices, entrepreneurs can:

- Reduce potential audit risks

- Minimize tax preparation stress

- Maximize potential tax deductions

- Ensure compliance with federal regulations

- Provide transparent financial documentation

Pro tip: Develop a consistent record-keeping system and digitize financial documents to streamline tax preparation and maintain regulatory compliance.

Risks of Poor or Neglected Bookkeeping

Neglecting proper bookkeeping can transform a promising small business into a financial disaster waiting to happen. Common bookkeeping mistakes can lead to devastating consequences that extend far beyond simple paperwork errors.

Financial mismanagement creates a ripple effect of potential risks that can compromise a business’s entire operational stability. Inaccurate record-keeping doesn’t just create administrative headaches – it can trigger serious financial and legal complications that threaten a company’s survival.

Potential risks of poor bookkeeping include:

- Incorrect tax reporting and potential IRS penalties

- Loss of critical tax deductions

- Compromised cash flow management

- Damaged credibility with lenders and investors

- Inability to track business performance accurately

- Increased vulnerability to financial fraud

- Potential legal and compliance issues

Small businesses are particularly vulnerable to bookkeeping challenges. Without systematic financial tracking, entrepreneurs risk making uninformed decisions that can drain resources and undermine long-term growth. The lack of accurate financial documentation can prevent businesses from:

- Securing loans or investment capital

- Understanding true profitability

- Identifying potential financial inefficiencies

- Creating realistic business strategies

- Maintaining competitive market positioning

Poor bookkeeping is like navigating without a map – you’re guaranteed to get lost and potentially run out of fuel before reaching your destination.

Pro tip: Invest in regular financial reviews and consider professional bookkeeping services to catch and correct potential record-keeping issues before they become critical problems.

Take Control of Your Small Business Finances with Expert Bookkeeping

Struggling to keep up with daily financial tracking or worried about tax preparation complexities discussed in the article Why Small Businesses Need Bookkeeping Services This is a challenge many small business owners face when managing bookkeeping on their own Kenworthy Bookkeeping understands these key pain points including the need for accurate record-keeping real-time financial insights and reliable tax season preparation Our team uses QuickBooks Online to offer streamlined bookkeeping services such as categorization bank reconciliations and detailed profit and loss reports to give you clarity and confidence in your business finances

Don’t let bookkeeping become an overwhelming burden Take advantage of professional support that transforms your financial data into a strategic tool for growth and compliance Visit schedule a consultation to get started and experience how effortless bookkeeping can empower your business Act now to regain control and build a trusted financial foundation with Kenworthy Bookkeeping

Frequently Asked Questions

Why is bookkeeping important for small businesses?

Accurate bookkeeping is vital for small businesses as it provides clear insights into financial performance, aids in tax preparation, and supports informed decision-making, ensuring business growth and sustainability.

What are the main bookkeeping methods available for small businesses?

Small businesses typically use two primary bookkeeping methods: single-entry bookkeeping, which is simpler and suitable for very small operations, and double-entry bookkeeping, which offers more detailed and accurate financial insights.

How can poor bookkeeping affect a small business?

Poor bookkeeping can lead to incorrect tax reporting, cash flow mismanagement, loss of tax deductions, increased vulnerability to fraud, and an overall inability to make informed business decisions, jeopardizing financial stability.

What are the legal requirements for bookkeeping in small businesses?

Small businesses are required to document all income, track expenses with receipts, maintain payroll records, preserve financial statements, and retain tax returns, typically for three to seven years to comply with legal regulations.

One Comment

Comments are closed.