Why updating financial policies is crucial for Kansas SMBs

Many small business owners in Kansas believe financial policies are permanent documents requiring minimal attention after initial creation. This misconception can expose businesses to compliance violations, operational delays, and costly penalties. As state regulations evolve and business operations expand, outdated policies become liabilities rather than protective frameworks. Kansas businesses face unique regulatory requirements that demand regular policy reviews and updates. This guide explains why maintaining current financial policies is essential for compliance, risk management, and operational efficiency, helping you protect your business while streamlining financial operations.

Table of Contents

- Key takeaways

- The evolving regulatory landscape in Kansas and why it demands policy updates

- Establishing effective review cycles and roles for your financial policies

- Risks of outdated financial policies and benefits of timely updates

- Leveraging internal controls, audits, and technology to streamline policy updates

- How Kenworthy Bookkeeping supports your financial policy updates

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Policy updates essential | Kansas evolving laws require current financial policies to reflect the latest rules and protect the business. |

| Thresholds matter now | The 2025 Consumer Credit Code changes raise the credit transaction threshold to 69,500 and expand supervised loan requirements. |

| Role clarity boosts accountability | Assign responsible parties such as the CFO to oversee policy reviews and updates. |

| Regular reviews reduce risk | Establish quarterly or annual review cycles to catch gaps before penalties or disruptions occur. |

The evolving regulatory landscape in Kansas and why it demands policy updates

Kansas businesses operate in a dynamic regulatory environment that requires constant vigilance. In 2025, Kansas enacted major Consumer Credit Code changes, notably raising credit thresholds and adjusting finance charges, requiring updated policies. These revisions significantly impact how small businesses structure their financial operations and credit relationships.

The Consumer Credit Code changes include several critical updates. The credit transaction threshold increased from $25,000 to $69,500, affecting which transactions fall under supervised loan requirements. Finance charge limits were adjusted to reflect current economic conditions. The scope of supervised loan licenses expanded to cover additional transaction types. These changes require immediate policy revisions for businesses extending credit or managing customer financing.

Key legislative changes affecting Kansas small businesses include:

- Credit transaction threshold raised to $69,500, expanding regulated transaction scope

- Finance charge limits adjusted for inflation and market conditions

- Supervised loan license requirements broadened to include more transaction types

- Enhanced disclosure requirements for consumer credit arrangements

- Stricter documentation standards for credit file maintenance

The Kansas state bank commissioner mandates that licensees adopt and maintain written policies demonstrating compliance with these new requirements. This directive carries significant weight:

“All licensees must adopt or update written policies and procedures that demonstrate compliance with the revised Consumer Credit Code provisions, including enhanced documentation standards and updated transaction thresholds.”

For Kansas small businesses, these regulatory shifts mean your existing financial policies likely contain outdated thresholds, incorrect procedures, or gaps in compliance coverage. Maintaining bookkeeping compliance Kansas City standards requires proactive policy updates that reflect current legal requirements. Businesses that delay updates risk operating under frameworks that no longer protect them legally or operationally.

The regulatory landscape continues evolving beyond credit code changes. Tax reporting requirements shift annually. Employment law updates affect payroll policies. Data security standards become more stringent. Each change demands corresponding policy adjustments to maintain full compliance and operational effectiveness.

Establishing effective review cycles and roles for your financial policies

Successful policy management requires structured review cycles and clear accountability. Financial policies should be reviewed quarterly or annually, with responsible parties like CFOs designated for oversight. The frequency depends on your business size, industry complexity, and regulatory exposure.

Quarterly reviews work best for businesses with high transaction volumes, multiple revenue streams, or significant regulatory obligations. These reviews catch compliance gaps early and allow rapid adjustments to changing requirements. Annual reviews suit smaller operations with stable regulatory environments and straightforward financial structures. However, even annual review schedules should include trigger events that prompt immediate policy evaluation, such as new legislation, business expansion, or operational changes.

Assigning clear accountability ensures policies receive consistent attention. Designate a finance lead, CFO, or controller as the primary policy owner. This person coordinates reviews, tracks regulatory changes, and implements updates. For businesses without dedicated finance staff, the owner or general manager must assume this responsibility, potentially with external bookkeeping support.

Follow this systematic approach to conduct effective policy reviews and updates:

- Schedule review sessions at consistent intervals, blocking dedicated time for thorough evaluation

- Gather current policies, recent regulatory updates, and operational change documentation

- Compare existing policy language against current legal requirements and business practices

- Identify gaps, outdated provisions, and areas requiring clarification or expansion

- Draft policy revisions with specific language addressing identified issues

- Review drafts with key stakeholders including bookkeepers, legal advisors, and operational managers

- Implement approved changes with clear communication to affected staff

- Document the review process, changes made, and implementation dates for audit trails

Pro Tip: Align policy reviews with your monthly financial review process to create natural touchpoints for evaluation. When you close monthly books, spend 15 minutes noting any operational friction or compliance questions that arose. These notes become valuable input for quarterly or annual policy reviews, ensuring updates address real business needs rather than theoretical concerns.

Integrating policy updates with business milestones creates natural review triggers. When you launch new products, enter new markets, or hire additional employees, evaluate whether existing policies adequately cover these changes. Regulatory announcement monitoring also helps. Subscribe to Kansas Department of Revenue updates, Small Business Administration bulletins, and industry association newsletters to catch relevant changes early.

Effective bookkeeping reviews small businesses conduct regularly reveal policy gaps through practical application. When your bookkeeper encounters unclear guidance or discovers processes that contradict written policies, these findings signal update needs. Treat operational friction as valuable feedback for policy improvement.

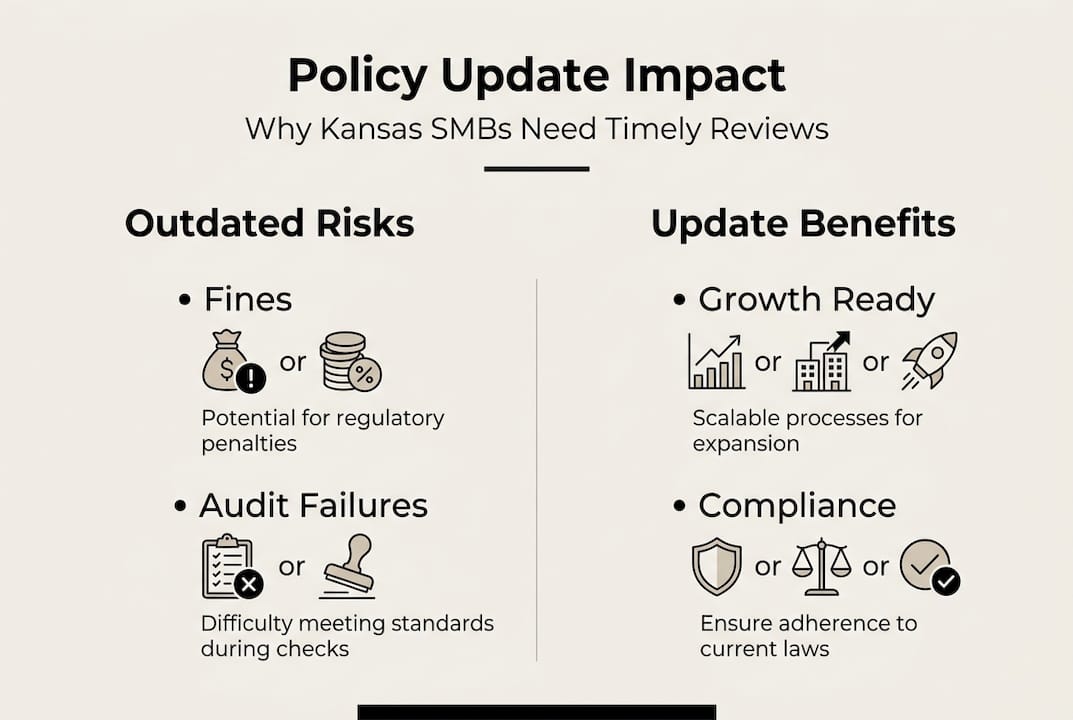

Risks of outdated financial policies and benefits of timely updates

Neglecting policy updates exposes Kansas small businesses to significant consequences. Noncompliance due to outdated policies can lead to fines and operational disruptions, as demonstrated in cases like Santander’s regulatory penalties. The risks extend beyond financial penalties to include operational disruptions, reputational damage, and strategic setbacks.

Regulatory penalties for noncompliance vary by violation type and severity. Updating policies helps avoid fines up to $500 per day for regulations like FTC Safeguards, ACA reporting, and wage increases. These daily fines accumulate rapidly, turning minor oversights into major financial burdens. Beyond direct penalties, noncompliance triggers costly audits, legal fees, and remediation expenses.

The severity of daily compliance fines cannot be overstated:

“Businesses face penalties up to $500 per day for violations of federal regulations including FTC Safeguards Rule, ACA reporting requirements, and state wage law compliance, with fines accumulating until full compliance is achieved.”

Common risks associated with outdated financial policies include:

- Regulatory fines and penalties ranging from hundreds to thousands of dollars daily

- Failed audits requiring expensive remediation and follow up examinations

- Operational disruptions from compliance gaps discovered during critical business activities

- Data breach vulnerabilities from outdated security and privacy policies

- Inaccurate financial reporting leading to poor business decisions

- Employee confusion and errors from contradictory or unclear guidance

- Lost business opportunities due to inability to demonstrate compliance to partners or lenders

- Increased insurance costs or coverage denial from poor compliance records

Operational risks often prove more damaging than direct penalties. When auditors discover policy gaps, they may halt operations until compliance is restored. Customer relationships suffer when data breaches occur due to inadequate security policies. Lending institutions deny credit applications from businesses unable to demonstrate sound financial controls. These indirect consequences compound over time, limiting growth and profitability.

Conversely, maintaining current policies delivers substantial benefits. Compliance becomes straightforward when policies accurately reflect current requirements. Your business finance checklist 2025 stays relevant and actionable. Risk mitigation improves as policies address emerging threats and vulnerabilities. Operational efficiency increases when staff follow clear, current guidance rather than navigating outdated or contradictory instructions.

Benefits of timely policy updates include:

- Simplified compliance through accurate reflection of current legal requirements

- Reduced audit risk and faster, smoother examination processes

- Enhanced operational efficiency from clear, current staff guidance

- Improved financial decision making based on accurate, compliant reporting

- Stronger business relationships with lenders, partners, and customers

- Lower insurance costs from demonstrated risk management

- Competitive advantages from reliable compliance reputation

- Peace of mind knowing your business operates within legal boundaries

Updated policies also position businesses for growth. When expansion opportunities arise, current policies provide the foundation for scaling operations compliantly. Acquisition discussions proceed smoothly when due diligence reveals well maintained financial controls. Strategic planning becomes more accurate when policies reflect actual operational realities rather than outdated assumptions.

Leveraging internal controls, audits, and technology to streamline policy updates

Smart businesses use systematic approaches to maintain current policies without overwhelming administrative burden. Post compliance, businesses should revise policies regularly using internal controls, audits, and technology to enhance stability and efficiency. These tools transform policy maintenance from reactive crisis management to proactive business protection.

Internal controls create checkpoints that reveal policy gaps during normal operations. Segregation of duties, approval hierarchies, and reconciliation procedures expose areas where written policies diverge from actual practice. When controls identify discrepancies, they signal policy update needs. Regular control testing during monthly or quarterly reviews provides continuous feedback on policy effectiveness.

Audits serve as comprehensive policy health checks. Internal audits conducted annually or semi annually evaluate whether policies cover all necessary areas, reflect current regulations, and align with actual business practices. External audits by CPAs or compliance specialists provide objective assessments and identify blind spots internal teams might miss. Both audit types generate specific recommendations for policy improvements.

Technology dramatically reduces the manual burden of policy maintenance. Compliance management software tracks regulatory changes, maps them to affected policies, and alerts designated staff when updates are needed. Document management systems maintain version control, ensuring everyone accesses current policy language. Automated workflows route policy drafts through review and approval processes efficiently.

| Approach | Pros | Cons | Time Investment |

|---|---|---|---|

| Manual policy tracking | Low cost, complete control, no technology learning curve | High error risk, time intensive, difficult to scale | 8-12 hours monthly |

| Spreadsheet based monitoring | Moderate cost, customizable, familiar tools | Manual data entry, version control challenges, limited automation | 4-6 hours monthly |

| Compliance software | Automated alerts, regulatory database access, workflow management | Subscription costs, learning curve, setup time required | 1-2 hours monthly after setup |

| Professional services | Expert guidance, comprehensive coverage, minimal internal time | Highest cost, less internal knowledge building | 30 minutes monthly coordination |

For Kansas small businesses, the right approach balances cost, complexity, and coverage. Start with enhanced manual systems using calendars and checklists to track review schedules and regulatory monitoring. As your business grows, migrate to spreadsheet based tracking that centralizes policy information and review histories. When administrative burden becomes significant, invest in compliance software or professional services.

Pro Tip: Many affordable compliance tools designed for small businesses cost less than $100 monthly and deliver significant time savings. Look for Kansas specific features or customizable platforms that track state regulations alongside federal requirements. Free trials let you test functionality before committing. Prioritize tools that integrate with your existing accounting software to minimize data entry and maximize efficiency.

Technology also improves policy communication and training. Cloud based policy repositories ensure staff always access current versions. Automated notifications alert employees when policies change. Online training modules help teams understand new requirements. These features reduce implementation friction and improve compliance consistency.

Combining internal controls, regular audits, and appropriate technology creates a sustainable policy maintenance system. You catch issues early through controls, validate comprehensiveness through audits, and reduce administrative burden through automation. This integrated approach helps you organize business finances success while maintaining compliance without overwhelming your team.

How Kenworthy Bookkeeping supports your financial policy updates

Maintaining current financial policies requires expertise, time, and systematic attention that many Kansas small business owners struggle to provide consistently. Kenworthy Bookkeeping specializes in helping businesses establish and maintain compliant financial policies tailored to Kansas regulations and your specific operational needs. Our team stays current on evolving state requirements, ensuring your policies reflect the latest legal standards without requiring you to monitor regulatory changes constantly.

We provide personalized consulting that evaluates your existing policies, identifies gaps or outdated provisions, and recommends specific updates aligned with current Kansas laws. Our regular review services integrate policy maintenance into your ongoing bookkeeping relationship, creating natural touchpoints for evaluation and updates. This proactive approach prevents compliance gaps before they become costly problems. Beyond policy documents, we help implement the internal controls and processes that make policies effective in daily operations. Ready to ensure your financial policies protect your business? Schedule a consultation to discuss your policy needs and discover how we can simplify compliance while strengthening your financial foundation.

Frequently asked questions

How frequently should I update my financial policies?

Most Kansas small businesses should review financial policies quarterly if they have complex operations or significant regulatory exposure, while simpler businesses can conduct thorough annual reviews. However, certain triggers demand immediate policy evaluation regardless of your regular schedule, including new legislation affecting your industry, significant business changes like expansion or new product lines, and operational issues revealing policy gaps. Staying aligned with Kansas state laws requires monitoring regulatory updates and adjusting policies promptly when changes affect your business.

What are the common risks of not updating financial policies regularly?

Outdated policies expose businesses to regulatory fines that can reach $500 daily for certain violations, failed audits requiring expensive remediation, and operational disruptions when compliance gaps halt critical business activities. Beyond direct penalties, neglected policies increase vulnerability to data breaches through inadequate security standards, enable financial mismanagement from unclear guidance, and damage business relationships when partners or lenders discover poor compliance practices. These risks compound over time, creating financial and operational problems that become increasingly difficult and expensive to resolve. Following a comprehensive business finance checklist 2025 helps identify and address policy gaps before they create serious problems.

How can Kenworthy Bookkeeping help with financial policy compliance?

Kenworthy Bookkeeping provides expert guidance on developing, reviewing, and updating financial policies specifically tailored to Kansas regulations and your business operations. We conduct periodic policy reviews integrated with your regular bookkeeping services, ensuring continuous compliance without requiring separate administrative processes. Our team helps automate compliance monitoring, streamline policy update workflows, and implement internal controls that make policies effective in daily operations. This comprehensive support reduces your risk exposure while minimizing the time you spend on compliance management. Schedule a consultation to learn how we can simplify your financial policy compliance and strengthen your business foundation.

What specific Kansas regulations affect small business financial policies?

Kansas small businesses must address several state specific requirements in their financial policies, including Consumer Credit Code provisions governing credit transactions and financing arrangements, state tax regulations covering sales tax collection and income tax reporting, employment laws affecting payroll and wage policies, and data security requirements for customer information protection. Additionally, businesses in regulated industries face sector specific requirements from Kansas agencies. Your financial policies must accurately reflect these Kansas requirements alongside federal regulations to ensure comprehensive compliance. Working with Kansas focused bookkeeping professionals ensures your policies address both state and federal obligations appropriately.

Can I use policy templates or do I need custom policies?

While policy templates provide useful starting frameworks, Kansas small businesses need customized policies that reflect their specific operations, industry requirements, and risk profile. Generic templates often contain provisions irrelevant to your business while omitting critical elements your situation requires. Effective customization involves adapting template language to your actual processes, adding Kansas specific regulatory requirements, incorporating your business structure and operational realities, and addressing unique risks your industry or business model faces. Professional guidance helps you efficiently customize templates rather than starting from scratch, balancing cost effectiveness with comprehensive coverage that truly protects your business.