Journal balancing explained: bookkeeping clarity for KC businesses

Many Kansas City home service business owners assume their books are fine as long as the numbers seem to add up at the end of the month. That assumption is costly. True journal balancing means ensuring total debits equal total credits across every entry and your overall trial balance, which is the foundation of double-entry bookkeeping. Without it, errors hide in plain sight, quietly distorting your cash flow, tax filings, and profit picture. By the end of this guide, you will understand exactly how journal balancing works, where mistakes happen most often, and how to build a reliable routine that keeps your books accurate and your business on solid ground.

Table of Contents

- What is journal balancing? Breaking down the basics

- Step-by-step: How journal balancing works in practice

- Trial balance: Your safeguard before closing the books

- Common pitfalls: Mistakes and edge cases in journal balancing

- Manual versus automated journal balancing: Pros, cons, and best fit

- How to master journal balancing in your Kansas City service business

- Get expert help with journal balancing and bookkeeping

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Balance every entry | Always ensure total debits and credits match in every journal entry to prevent errors. |

| Monthly trial balance | Run a trial balance every month to detect problems early and support clear cash flow. |

| Watch for hidden errors | A balanced trial balance can still hide mistakes—always check for omissions and reconcile sub-ledgers. |

| Automate and review | Use software to automate routine checks but manually review exceptions and unusual items regularly. |

What is journal balancing? Breaking down the basics

Now that you are aware of the risks in assuming your books are balanced, let us define exactly what journal balancing means for your business.

Journal balancing is the process of confirming that total debits equal total credits in every journal entry you record. This is the core principle of double-entry bookkeeping, a system where every financial transaction affects at least two accounts simultaneously. Think of it as a built-in check: money never just appears or disappears, it always moves from one account to another.

For home service businesses in Kansas City, this matters more than you might expect. You are dealing with frequent transactions: service calls, material purchases, subcontractor payments, and customer invoices. Each one must be recorded correctly or your books drift out of alignment fast. Learning the small business bookkeeping basics gives you the foundation to manage this volume with confidence.

Here is what journal balancing covers in practice:

- Every transaction is recorded as both a debit and a credit

- The total of all debits must always equal the total of all credits

- Each entry affects at least two separate accounts

- Errors in one entry can cascade into your financial reports

- Consistent balancing prevents surprises at tax time

“Accurate journal entries are not just a bookkeeping formality. They are the data your entire financial picture depends on.”

Step-by-step: How journal balancing works in practice

With the basics clear, let us walk through the exact process and tools that make journal balancing straightforward, even when business gets busy.

The key mechanics of journal balancing follow a clear sequence: identify the accounts affected, apply debit and credit rules correctly, verify that totals match, and then post to the ledger. Skipping any step is where errors begin.

Here is the four-step process for a typical service business transaction:

- Set up your chart of accounts. Organize accounts by category: assets, liabilities, equity, revenue, and expenses. This is your map.

- Record the transaction with debits and credits. For example, when you complete a $500 HVAC service call and receive payment, debit your cash account $500 and credit your service revenue account $500.

- Post entries to the general ledger. Transfer each journal entry to the correct ledger account so balances stay current.

- Prepare a trial balance. List all account balances and confirm total debits equal total credits before closing the period.

| Step | Action | Common mistake |

|---|---|---|

| Chart setup | Categorize all accounts | Missing expense categories |

| Record entry | Apply debit and credit | Entering same side twice |

| Post to ledger | Transfer to account | Skipping the posting step |

| Trial balance | Verify totals match | Running it only at year-end |

For home service bookkeeping tips specific to your industry, reviewing entries daily rather than weekly catches problems before they compound.

Pro Tip: Set aside 10 minutes at the end of each workday to review that day’s entries. Catching a misposted transaction the same day takes two minutes to fix. Catching it three months later can take hours.

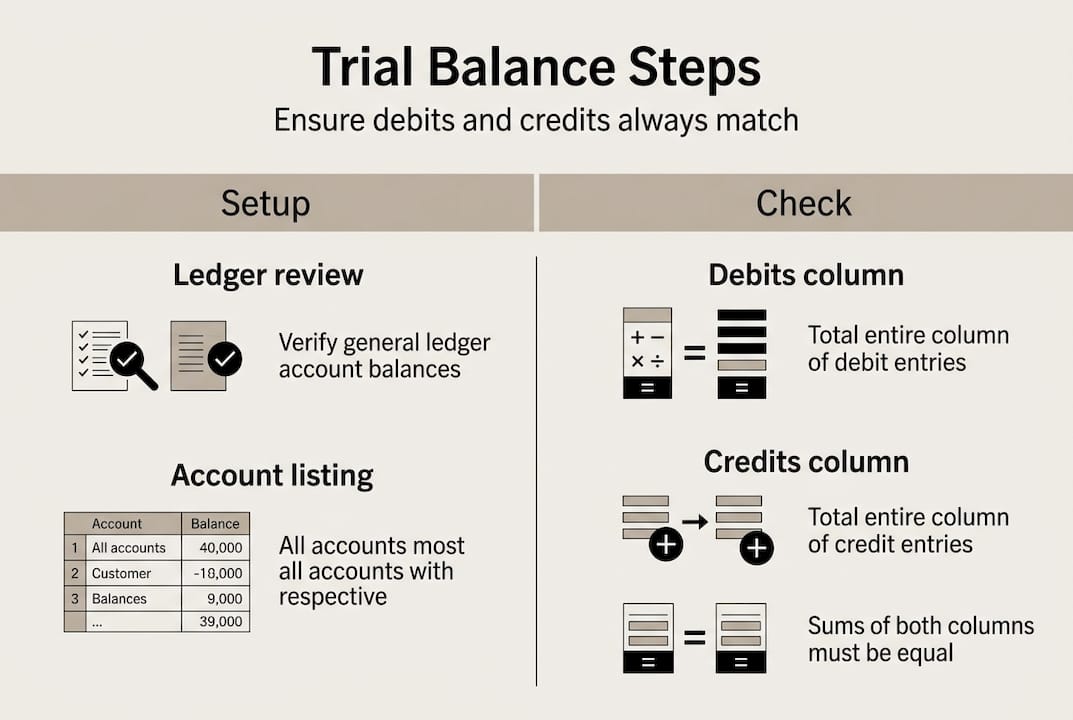

Trial balance: Your safeguard before closing the books

Once daily entries are made, you need a higher-level check. This is where the trial balance comes in.

A trial balance lists every ledger account’s ending balance in two columns: debits and credits. When the columns match, your books are in balance for that period. Running this monthly is especially important for home service businesses in Kansas City, where seasonal demand creates cash flow swings that can mask recording errors.

Here is a simplified trial balance example:

| Account | Debit | Credit |

|---|---|---|

| Cash | $8,200 | |

| Accounts receivable | $3,400 | |

| Equipment | $12,000 | |

| Accounts payable | $2,100 | |

| Service revenue | $18,500 | |

| Operating expenses | $7,000 | |

| Totals | $30,600 | $30,600 |

However, a balanced trial balance does not mean your books are error-free. A balanced trial balance can still contain omission errors, where a transaction was never recorded at all, or compensating errors, where two mistakes cancel each other out. Both leave your totals equal but your data wrong.

To catch what the trial balance misses, pair it with these steps:

- Reconcile your bank statements every month

- Review accounts receivable and payable aging reports

- Compare current period totals to prior months for unusual spikes

- Use account reconciliation steps as a monthly habit

When you streamline your bookkeeping with a consistent monthly routine, you catch the vast majority of issues before they affect your decisions.

Common pitfalls: Mistakes and edge cases in journal balancing

Even expertly run books can mislead you. Here is where many owners get tripped up, despite best efforts.

The most dangerous errors are the ones that do not trigger an imbalance. Omission and compensating errors are exactly this type: your trial balance looks fine, but a transaction was either never recorded or recorded incorrectly on both sides. These require manual review to catch, not just a software check.

Other common pitfalls include:

- Multicurrency transactions. If you pay a supplier in a different currency, you need additional steps to convert and balance those entries correctly.

- Suspense accounts. These are temporary holding accounts used when you are unsure where to post a transaction. Leaving entries in suspense too long creates confusion and imbalance risk.

- Intercompany accounts. If you operate more than one entity, transactions between them require careful matching on both sides.

- No imbalance threshold. Set a flag for any discrepancy over 1% of your monthly revenue. Small gaps add up.

Pro Tip: Do not rely solely on your software’s green checkmark. Review your bookkeeping success checklist monthly and manually inspect any account that shows unusual activity. Software catches math errors. It does not catch judgment errors.

Understanding the bookkeeping audit role also helps you prepare for situations where your records face external scrutiny.

Manual versus automated journal balancing: Pros, cons, and best fit

Navigating those pitfalls hinges on having the right process. Should you trust manual methods, or is it time for automation?

Manual verification adds scrutiny and helps you catch subtle errors that software overlooks. But for a busy home service business processing dozens of transactions weekly, pure manual review is risky and time-consuming. Automated systems prevent posting unbalanced entries in the first place, which is a significant safeguard.

| Method | Strengths | Weaknesses |

|---|---|---|

| Manual | Catches judgment errors, high scrutiny | Slow, error-prone at volume |

| Automated | Fast, prevents math errors, scalable | Misses omissions and logic errors |

| Hybrid | Best of both, practical for growth | Requires clear process design |

For most Kansas City service businesses, a hybrid approach works best. Prioritize automation for routine, high-volume transactions and apply manual review to high-value entries, unusual transactions, and month-end closing.

“The goal is not to choose between manual and automated. It is to use each where it performs best, so nothing falls through the cracks.”

If managing this balance feels like too much on top of running your business, outsourcing bookkeeping to a specialist is a practical and cost-effective option.

How to master journal balancing in your Kansas City service business

You are ready to put these concepts into action. Here is how to make routine journal balancing second nature for your business.

A balanced trial balance is a starting point, not a finish line. Reconciling sub-ledgers and reviewing outliers is what separates accurate books from books that just look accurate. Build your routine around these three time frames:

- Daily: Review all entries from the day. Confirm debits equal credits. Flag anything unusual.

- Weekly: Reconcile accounts receivable and payable. Check for entries sitting in suspense accounts.

- Monthly: Prepare your trial balance. Run bank reconciliation. Compare totals to prior months and investigate spikes.

| Task | Frequency | Why it matters |

|---|---|---|

| Entry review | Daily | Catches errors while memory is fresh |

| Sub-ledger reconciliation | Weekly | Prevents aging errors in AR and AP |

| Trial balance | Monthly | Confirms overall balance before close |

| Bank reconciliation | Monthly | Catches omissions and bank errors |

| Outlier review | Monthly | Flags unusual activity early |

When your books are accurate, interpreting your financial statements becomes straightforward. You can use your P&L and cash flow data for real bookkeeping and planning decisions, not just compliance. That is the real payoff of getting journal balancing right. Understanding the importance of bookkeeping goes beyond tax season. It gives you the clarity to grow with confidence.

Get expert help with journal balancing and bookkeeping

If you want journal balancing to be even easier, specialized support is right at your fingertips.

At Kenworthy Bookkeeping, we treat your books like they are our own business. We work with Kansas City home service businesses every day, handling categorization, bank reconciliations, P&L reports, and tax season preparation so you can focus on the work you do best. Our approach is tailored to the real demands of service businesses: high transaction volume, seasonal cash flow, and the need for clear, actionable insights you can actually use.

You do not have to figure out journal balancing on your own. Whether you want a professional review of your current process or full-service bookkeeping support, we are here to help. Schedule a bookkeeping consult with our team and take the first step toward books you can trust, every single month.

Frequently asked questions

Why is journal balancing important for small businesses?

Journal balancing ensures every dollar is accurately recorded by confirming that total debits equal credits in every entry, which prevents financial errors from distorting your reports and decisions.

How often should I prepare a trial balance?

You should run a trial balance monthly so you can catch mistakes early and keep a clear picture of your cash flow throughout the year.

Can accounting software fully replace manual checks during journal balancing?

No. While software prevents posting unbalanced entries automatically, manual review is still essential for catching omission errors, logic mistakes, and unusual high-value transactions.

What errors can a trial balance miss?

A trial balance can miss omissions and compensating errors, where a transaction was never recorded or where two offsetting mistakes leave the totals equal but the underlying data wrong.

Should I reconcile sub-ledgers separately when balancing journals?

Yes. Reconciling sub-ledgers like accounts receivable and payable is a necessary step beyond the trial balance to confirm your books are truly accurate, not just mathematically balanced.