What is financial risk management: a small business guide

Nearly half of all small businesses fail within their first five years, often due to unmanaged financial risks that could have been prevented. Many Kansas business owners mistakenly believe financial risk management is only about insurance or banking jargon, when it’s actually a practical toolkit for protecting your business from monetary threats. Understanding how to identify and control financial risks can dramatically improve your business’s fiscal stability and longevity. This guide explains what financial risk management really means, the specific risks Kansas small businesses face, and actionable strategies you can implement today to safeguard your business interests.

Table of Contents

- Key takeaways

- Understanding financial risk management in small business

- Common financial risks faced by Kansas small businesses

- Financial risk management strategies for Kansas small businesses

- Get expert help managing your small business finances

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| FRM identifies and reduces risk | Financial risk management helps small businesses identify and reduce monetary uncertainties that threaten profitability. |

| Kansas resources | SCKEDD and Network Kansas offer tailored solutions to lower credit risk without requiring excessive personal guarantees. |

| Risk controls improve survival | Implementing risk controls improves business survival and financial health. |

| Proactive strategies | Proactive strategies include maintaining accurate bookkeeping, purchasing appropriate insurance, and using financial forecasting to anticipate challenges. |

| Informed decisions and confidence | Understanding risks leads to better decisions and increased confidence in managing your business finances. |

Understanding financial risk management in small business

Financial risk management (FRM) means identifying, analyzing, and mitigating risks that can cause financial loss to your business. It’s not a complex corporate concept reserved for Wall Street. Think of it as your business’s financial immune system, constantly scanning for threats and building defenses against them.

Small business owners often misunderstand FRM as simply buying insurance or maintaining good banking relationships. While those elements matter, true financial risk management is a comprehensive process that touches every aspect of your business finances. It includes monitoring cash flow patterns, evaluating customer creditworthiness, planning for market changes, and establishing internal controls to prevent errors or fraud.

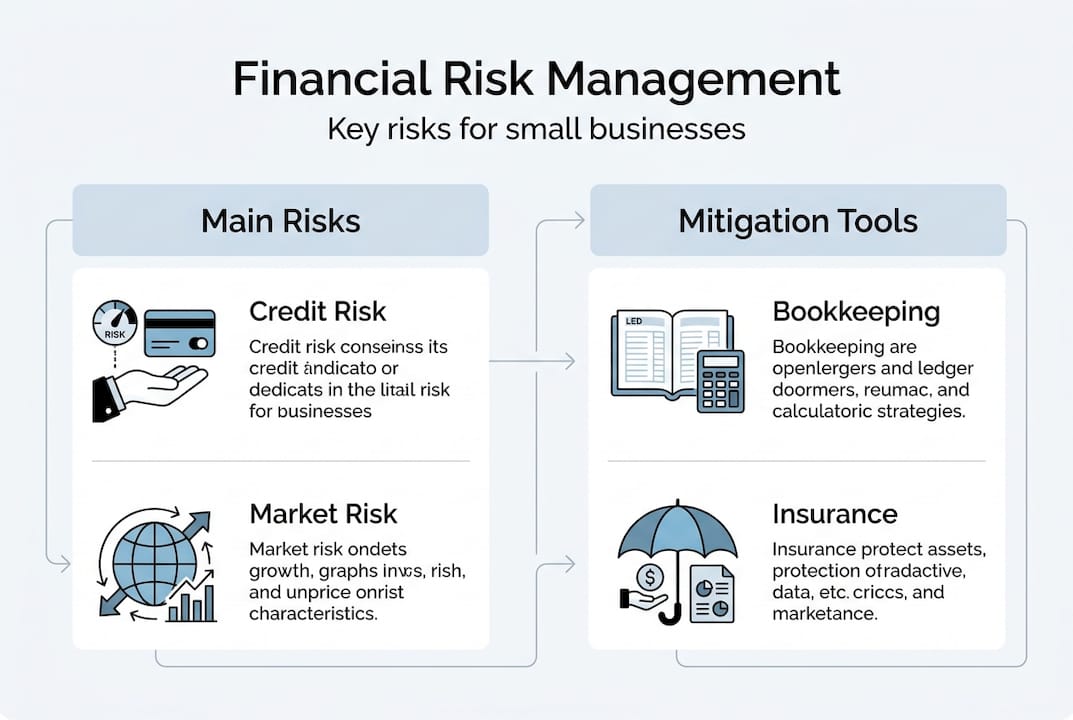

The main types of financial risks include:

- Credit risk: the possibility that customers or borrowers won’t pay what they owe

- Market risk: changes in economic conditions, customer demand, or competitive landscape that affect revenue

- Liquidity risk: inability to access cash when needed to cover expenses or seize opportunities

- Operational risk: financial losses from inadequate processes, human errors, or system failures

Small businesses face unique FRM challenges compared to large corporations. You operate with limited resources, tighter margins, and less access to sophisticated financial tools. A single bad debt or cash flow disruption can threaten your entire operation in ways that would barely register for a Fortune 500 company. Research shows SMEs often underinvest in enterprise risk management despite clear evidence these practices improve business outcomes.

Effective FRM improves your decision-making by providing clarity about potential downsides before you commit resources. When you understand the risks associated with taking on a new client, expanding to a new location, or purchasing equipment, you can structure deals to protect yourself or decide the opportunity isn’t worth the exposure. This strategic awareness separates businesses that thrive from those that merely survive.

Common financial risks faced by Kansas small businesses

Kansas small businesses encounter specific financial risks shaped by local economic conditions and market dynamics. Recognizing these threats is the first step toward protecting your business.

Credit risk presents itself when you struggle to obtain affordable financing or when customers delay payments. Many Kansas small businesses find traditional bank loans difficult to access without substantial collateral or perfect credit histories. This forces owners to either forgo growth opportunities or accept unfavorable terms that strain cash flow. On the customer side, extending credit to clients who pay late or default creates cash shortages that ripple through your operations.

Cash flow risk stems from irregular payment cycles and seasonal revenue fluctuations common in Kansas markets. You might have profitable months on paper while struggling to make payroll because receivables haven’t arrived. This mismatch between income timing and expense obligations creates constant stress and limits your ability to invest in growth or handle unexpected costs. Financial forecasting helps anticipate these patterns, but many small businesses lack the systems to implement it effectively.

Market risk includes changes in local economic conditions, shifts in customer preferences, and competitive pressures. Kansas’s economy includes agricultural, manufacturing, and service sectors that each face distinct market dynamics. A downturn in farming can affect Main Street retail. New competitors or changing consumer behaviors can erode your customer base faster than you can adapt. These external forces are largely beyond your control, but you can prepare for them.

Operational risk emerges from internal weaknesses in your financial processes. Bookkeeping errors, lack of financial controls, inadequate documentation, or poor inventory management all create opportunities for losses. When your bookkeeping practices lack rigor, you might miss fraudulent transactions, miscalculate taxes, or make decisions based on inaccurate financial data. These mistakes compound over time, creating problems that become expensive to fix.

Legal and compliance risks affect Kansas small businesses through changing tax regulations, employment laws, and industry-specific requirements. Failing to comply with state or federal regulations can result in penalties, legal fees, and reputational damage that threaten your business viability.

Pro Tip: Leveraging local Kansas resources like SCKEDD helps mitigate credit risk by providing access to financing with more favorable terms and lower personal guarantee requirements than traditional banks typically offer.

Financial risk management strategies for Kansas small businesses

Implementing practical risk management strategies doesn’t require expensive consultants or complex systems. Start with these proven approaches tailored for small business realities.

-

Establish solid bookkeeping and financial controls as your foundation. Accurate, timely financial records let you spot problems early when they’re still manageable. Implement separation of duties so no single person controls all aspects of financial transactions. Reconcile bank accounts monthly. Review financial statements regularly to identify unusual patterns. These basic controls prevent most operational risks and provide the data you need for informed decisions.

-

Use financial planning and forecasting to anticipate cash flow challenges before they become crises. Project your income and expenses for the next 90 days, then compare actual results to your projections. This practice reveals seasonal patterns, helps you plan for slow periods, and identifies when you’ll need additional financing. Financial planning transforms from abstract concept to practical tool when you use it to answer specific questions about your business’s future.

-

Leverage Kansas-specific loan programs designed to reduce credit risk for small businesses. The SCKEDD midsize loan program offers financing up to $400,000 with terms more favorable than conventional banks, specifically targeting businesses that fall between microloans and traditional commercial lending. Network Kansas provides consulting and connections to capital sources throughout the state. These resources exist specifically to help Kansas businesses access affordable financing.

-

Purchase appropriate insurance to transfer risks you can’t effectively manage internally. General liability, property, professional liability, and business interruption insurance protect against events that could otherwise destroy your business. Review coverage annually as your business grows and risks evolve. Insurance premiums represent a predictable expense that prevents unpredictable catastrophic losses.

-

Regularly review and update your risk management plans as your business changes. What worked when you had five employees and $500,000 in revenue won’t suffice when you reach 20 employees and $2 million. Schedule quarterly reviews of your major financial risks, control systems, and mitigation strategies. Adjust as needed based on changes in your business, market, or regulatory environment.

| Strategy | Primary risk addressed | Implementation difficulty | Cost |

|---|---|---|---|

| Professional bookkeeping | Operational risk | Low | Moderate |

| Cash flow forecasting | Liquidity risk | Medium | Low |

| Kansas loan programs | Credit risk | Medium | Low to moderate |

| Business insurance | Market and operational risks | Low | Moderate to high |

| Financial controls | Operational risk | Low to medium | Low |

Research confirms that risk mitigation through tailored financial tools and local programs significantly improves small business survival odds, particularly when businesses commit to ongoing monitoring rather than one-time implementations.

Pro Tip: Strong bookkeeping practices serve as the foundation for all other risk management strategies because they provide the accurate, timely data you need to identify emerging risks and measure the effectiveness of your mitigation efforts.

Get expert help managing your small business finances

Implementing effective financial risk management requires accurate data, strategic thinking, and consistent execution. Professional bookkeeping ensures your financial records provide the reliable foundation needed to identify risks early and measure results accurately. When your books are current and correct, you can spot unusual patterns, track key metrics, and make decisions with confidence.

Expert financial consulting tailors risk strategies to your specific Kansas business context, industry dynamics, and growth stage. Consultants bring experience from working with hundreds of businesses, helping you avoid common pitfalls and implement proven solutions faster than trial and error allows. Taking action with professional support improves both your confidence in financial decisions and the actual stability of your business finances. You don’t have to navigate financial risks alone when experienced partners can help you build systems that protect and grow your business.

Frequently asked questions

What key financial risks should small businesses monitor?

Small businesses should actively monitor credit risk from customers who may not pay, liquidity risk from cash flow timing mismatches, market risk from economic changes, and operational risk from internal control weaknesses. Focus your attention on the risks most likely to occur in your specific industry and business model. Prioritize monitoring the risks that would cause the most damage if they materialized, even if their probability seems low.

How can small businesses in Kansas access financial risk management resources?

Kansas small businesses can access specialized resources through SCKEDD, which offers midsize loans with favorable terms, and Network Kansas, which provides consulting and capital connections statewide. The Kansas Small Business Development Center offers free consulting on financial planning and risk management. Local chambers of commerce and industry associations also provide networking opportunities to learn from other business owners’ experiences. These resources exist specifically to help Kansas businesses succeed, so take advantage of them.

What role does bookkeeping play in managing financial risk?

Bookkeeping provides the accurate, timely financial data essential for identifying and monitoring risks before they become crises. Proper bookkeeping practices let you spot unusual transactions, track key performance indicators, reconcile accounts to catch errors, and generate reports that reveal trends. Without solid bookkeeping, you’re essentially flying blind, making decisions based on gut feel rather than facts. Quality bookkeeping transforms financial risk management from theoretical concept to practical daily practice.

Are there affordable strategies to reduce credit and cash flow risk?

Yes, several affordable strategies effectively reduce these common risks. Implement clear payment terms and follow up promptly on overdue accounts to improve collections. Use deposit requirements for large orders to reduce exposure. Negotiate better payment terms with suppliers to align cash outflows with inflows. Build a cash reserve equal to at least one month of operating expenses to buffer against timing gaps. These strategies cost little to implement but significantly reduce your vulnerability to credit and cash flow problems.

How often should financial risk management plans be reviewed?

Review your financial risk management plans quarterly at minimum, with more frequent reviews during periods of significant change like rapid growth, market disruption, or economic uncertainty. Annual reviews are insufficient because risks evolve faster than yearly cycles in today’s business environment. Each quarterly review should assess whether identified risks have changed in likelihood or impact, whether new risks have emerged, and whether your mitigation strategies remain effective. Adjust your plans based on what the data shows rather than maintaining outdated assumptions.