Double entry accounting: Secure finances for Kansas businesses

TL;DR:

- Double entry accounting ensures accurate, balanced financial records vital for business growth and compliance.

- It involves recording each transaction in at least two accounts, maintaining the fundamental equation.

- Regular checks and routines are essential to prevent errors and keep books trustworthy for decision-making.

Many Kansas small business owners assume double entry accounting is something only large corporations need. That assumption can cost you. Without a reliable system for recording every transaction, your books become a guessing game, and guessing is expensive when tax season arrives or a lender asks for your financials. Double-entry accounting is the foundation of accurate, trustworthy bookkeeping, and it is more accessible than most people think. This guide walks you through what it is, how it works, and why it matters for your Kansas small business right now.

Table of Contents

- What is double entry accounting?

- Single entry vs. double entry: Key differences for your business

- The double entry process: How transactions really work

- Common errors and checks in double entry accounting

- How double entry accounting empowers your Kansas small business

- What most guides miss about double entry accounting

- Get personalized support with your Kansas business’s bookkeeping

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Foundation of business finance | Double entry accounting gives you clarity and control over your finances. |

| Prevents costly errors | Built-in checks and regular reconciliation help you catch problems early. |

| Essential for compliance | Double entry enables accurate reporting for audits, taxes, and loans. |

| Adaptable for all sizes | Small businesses in Kansas benefit from adopting double entry early, not just large firms. |

What is double entry accounting?

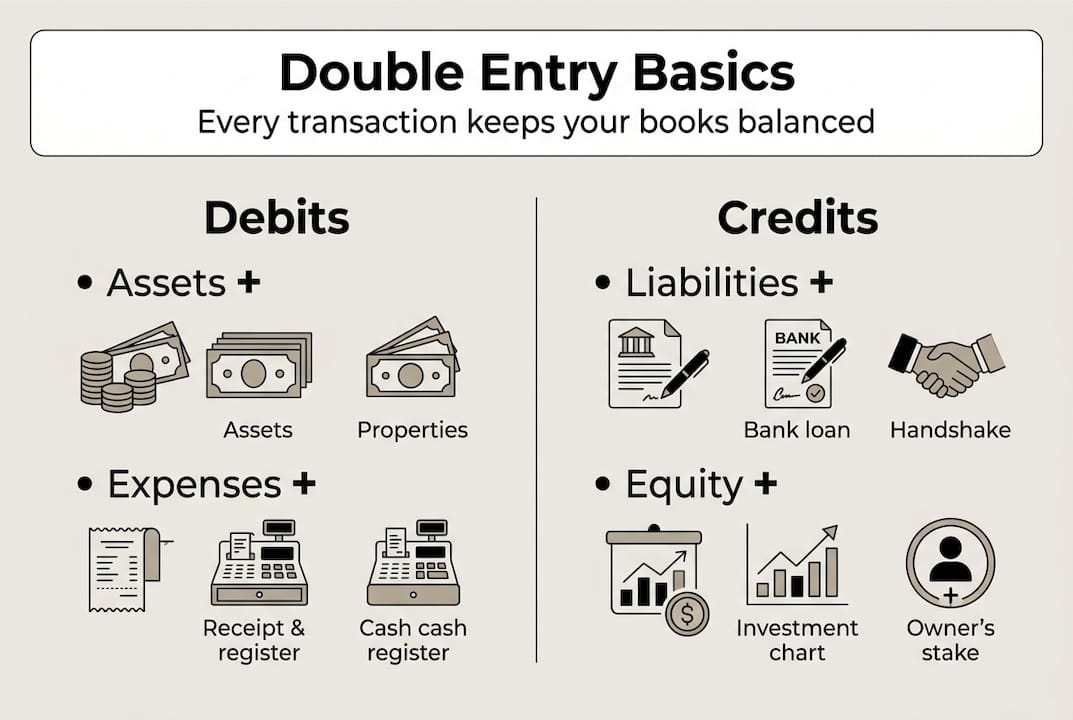

Double entry accounting can sound intimidating, but the core idea is straightforward. Every financial transaction your business makes gets recorded in at least two accounts: one as a debit and one as a credit. This keeps your books balanced at all times.

The system is built on one equation: Assets = Liabilities + Equity. Every transaction must keep this equation in balance. If you buy a piece of equipment, your assets go up and either your cash (an asset) goes down or your liabilities go up. Both sides of the equation stay equal. Double-entry accounting ensures the accounting equation remains balanced with every entry you make.

Here is a simple example of how a transaction looks under double entry:

| Transaction | Debit | Credit |

|---|---|---|

| Buy $500 of supplies with cash | Supplies (Asset) +$500 | Cash (Asset) -$500 |

| Take out a $2,000 loan | Cash (Asset) +$2,000 | Loan Payable (Liability) +$2,000 |

| Receive $1,000 from a client | Cash (Asset) +$1,000 | Revenue (Equity) +$1,000 |

Every row balances. That is the whole point.

Key benefits for small businesses:

- Catches errors before they become costly problems

- Produces accurate profit and loss reports

- Supports clean, audit-ready records

- Makes tax preparation faster and less stressful

- Gives lenders and investors confidence in your financials

- Supports strong bookkeeping compliance practices from day one

Pro Tip: Even a small transposition error, like recording $540 instead of $450, creates an imbalance your trial balance will catch. That built-in check is one of the biggest advantages double entry has over simpler systems.

Single entry vs. double entry: Key differences for your business

Single entry accounting records each transaction once, usually as income or an expense in a single column. It works like a personal checkbook register. It is simple, fast, and fine for a freelancer tracking a handful of transactions each month.

But as your business grows, single entry starts to show its limits. It does not track assets, liabilities, or equity. It cannot produce a balance sheet. And it does not meet compliance standards required for GAAP reporting or most business loans. Single entry records once and suits very small or simple businesses, while double entry is more accurate and required for growth and compliance.

| Feature | Single entry | Double entry |

|---|---|---|

| Accuracy | Limited | High |

| Error detection | Difficult | Built-in |

| Balance sheet | No | Yes |

| Loan readiness | Weak | Strong |

| GAAP compliance | No | Yes |

| Audit support | Poor | Excellent |

Double entry is the industry standard for a reason. Banks expect it. Auditors rely on it. And if you ever want to bring on a partner, sell your business, or apply for a line of credit, your financials need to reflect it. You can also review bookkeeping audits to understand what reviewers look for in your records.

Signs it is time to switch to double entry:

- Your revenue has grown beyond a few thousand dollars per month

- You have employees, inventory, or business loans

- You want to apply for financing or attract investors

- You are preparing for your first formal audit or tax review

- You want accurate P&L reports to guide business decisions

Pro Tip: Switching to double entry early is far easier than converting years of single entry records later. Set up the right system now, and your future self will thank you.

The double entry process: How transactions really work

Let’s make this concrete. Say you run a small landscaping company in Overland Park and you spend $300 cash on new gardening supplies. Here is what happens in a double entry system.

First, you identify the two accounts affected: Supplies (an asset account) and Cash (also an asset account). Supplies increases because you now own more inventory. Cash decreases because you spent money. You record a debit to Supplies for $300 and a credit to Cash for $300. The books stay balanced.

Double entry ensures accounts remain balanced and accurate for every report you generate. That accuracy is what makes your financial statements reliable.

Here is the standard process for recording any transaction:

- Identify the transaction. What happened? What did money touch?

- Determine the accounts affected. Which two (or more) accounts are involved?

- Decide debit or credit. Assets and expenses increase with debits. Liabilities, equity, and revenue increase with credits.

- Post to the journal. Record the entry with date, accounts, and amounts.

- Post to the ledger. Transfer journal entries to individual account ledgers.

- Prepare a trial balance. Add up all debits and credits to confirm they match.

Good journal balancing practices keep your records clean and your reports trustworthy throughout the month.

Pro Tip: Software like QuickBooks Online automates most of these steps. But knowing the flow means you can spot when something looks off, even if the software does not flag it right away.

Common errors and checks in double entry accounting

Double entry is a strong system, but it is not foolproof. Mistakes happen, especially when you are managing a business and bookkeeping at the same time. Knowing what to watch for puts you in control.

The most common double entry errors include:

- Swapping debits and credits (recording a debit where a credit belongs)

- Posting to the wrong account (office supplies charged to equipment, for example)

- Entering the wrong dollar amount

- Missing a transaction entirely

- Duplicating an entry by accident

These errors can slip through unnoticed until you try to reconcile your accounts or prepare a tax return. That is why regular checks matter. Useful account reconciliation tips can help you build a routine that catches problems early.

Checks to run regularly:

- Monthly bank reconciliation to match your records to your bank statement

- Trial balance review to confirm debits equal credits

- Account-by-account ledger review each quarter

- Comparison of P&L reports month over month to spot unusual changes

“A trial balance confirms arithmetic accuracy but does not catch all errors, such as entries posted to the wrong account. Regular reconciliations are essential for complete accuracy.” Investopedia

This is an important point. A balanced trial balance feels reassuring, but it does not mean everything is correct. Two wrong entries that cancel each other out will not show up as an imbalance. That is why reconciliation goes deeper than math.

If you do find an error, fix it promptly. Correcting mistakes right away keeps your records clean for tax prep and reduces the stress of fixing bookkeeping errors later in the year.

How double entry accounting empowers your Kansas small business

Double entry accounting is not just a technical requirement. It is a practical tool that gives you real visibility into your business finances. When your books are accurate, you make better decisions, plain and simple.

Here is what double entry does for Kansas small businesses:

- Gives you a clear picture of cash flow, assets, and liabilities at any time

- Produces reliable P&L reports so you know if you are actually profitable

- Prepares you for bank loans or lines of credit with solid financial statements

- Supports accurate tax filings and reduces the risk of costly errors

- Keeps you aligned with account reconciliation best practices

- Positions your business for growth with records that scale alongside you

Here is a fact worth knowing: the double entry system has been the foundation of modern business finance since the 14th century. It has outlasted every accounting trend because it works. Merchants in Renaissance Italy used it to manage trade across continents. You can use it to manage your Kansas City service business with the same confidence.

Proactive bookkeeping is not about being perfect. It is about staying informed. When you understand where your money is going and why your accounts look the way they do, you lead your business with clarity instead of anxiety. Reviewing bookkeeping compliance Missouri guidance can also help you stay current with regional requirements as your business grows.

What most guides miss about double entry accounting

Most articles explain the rules of double entry accounting clearly enough. What they rarely address is the gap between understanding the system and actually maintaining it under the daily pressure of running a small business.

Knowing that debits equal credits is not the hard part. The hard part is recording every transaction consistently, week after week, when you are also managing clients, employees, and operations. That is where most small business owners fall behind, not because they do not understand the system, but because life gets in the way.

Software helps significantly. But software does not think for you. It will not question whether a charge belongs in meals or marketing. It will not notice that a vendor payment was entered twice. Human oversight, even just a monthly review, is what turns good software into trustworthy books.

Double entry accounting works best as a discipline, not just a process. Building a routine around reconciliation steps is what separates businesses with clean, reliable financials from those scrambling every April. The system is only as strong as the habits behind it.

Get personalized support with your Kansas business’s bookkeeping

Understanding double entry accounting is a great first step. Putting it into consistent practice is where the real value shows up for your business.

At Kenworthy Bookkeeping, we handle your books like they are our own, using QuickBooks Online to keep your records accurate, balanced, and ready for tax season. From categorization and bank reconciliations to P&L reports and audit prep, we give Kansas small business owners the clarity and confidence they deserve. Schedule your bookkeeping consultation today and let us take the stress out of your finances so you can focus on growing your business.

Frequently asked questions

Is double entry accounting required for small businesses in Kansas?

Double entry is not legally required for all Kansas small businesses, but it is strongly recommended for accurate records, loan applications, and compliance. As your business grows, double-entry becomes essential for meeting lender and regulatory expectations.

What is the main benefit of double entry accounting over single entry?

Double entry gives you a full view of your finances, making errors easier to spot and keeping your books balanced. The accounting equation stays balanced with every transaction, which single entry cannot guarantee.

How do I know if I made a double entry bookkeeping mistake?

Unbalanced ledgers or a trial balance that does not add up are clear warning signs. Regular reconciliations are essential for catching errors that arithmetic checks alone might miss.

Can software handle double entry accounting for me?

Most modern bookkeeping software automates double entry recording, but reviewing entries for accuracy is still important. Understanding the flow helps you catch mistakes that automation may overlook.