Understanding Debits and Credits: A Guide for Small Businesses

Many small business owners confuse debits and credits with bank transactions, leading to costly bookkeeping and tax mistakes. In banking, a debit means money leaving your account and a credit means money coming in. But in bookkeeping, debits and credits work completely differently. This confusion costs businesses real money. Understanding the true meaning of debits and credits is essential for accurate financial records, tax compliance, and smart business decisions. This guide will explain everything you need to know, with clear examples and practical rules you can apply immediately.

Table of Contents

- What are debits and credits? The core bookkeeping rule explained

- Why mastering debits and credits matters for small businesses

- Debit and credit rules: Quick-reference table for business owners

- Common scenarios: How debits and credits work in real-life transactions

- Pitfalls and errors: How to avoid bookkeeping mistakes with debits and credits

- Taking control: Best practices for accurate bookkeeping in Kansas and Missouri

- Get bookkeeping support: Take the next step for your business

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Debits and credits rules | Assets and expenses increase on debit, while liabilities, equity, and revenue increase on credit. |

| Avoid costly mistakes | Misunderstanding debits and credits leads to errors, fines, and poor business decisions. |

| Apply in real life | Use basic rules and sample transactions to stay accurate in everyday business bookkeeping. |

| Local compliance | In Kansas and Missouri, book accuracy directly affects tax obligations and audit risks. |

What are debits and credits? The core bookkeeping rule explained

Now that you know confusion is common, let’s lay the foundation by defining debits and credits as they really work in bookkeeping.

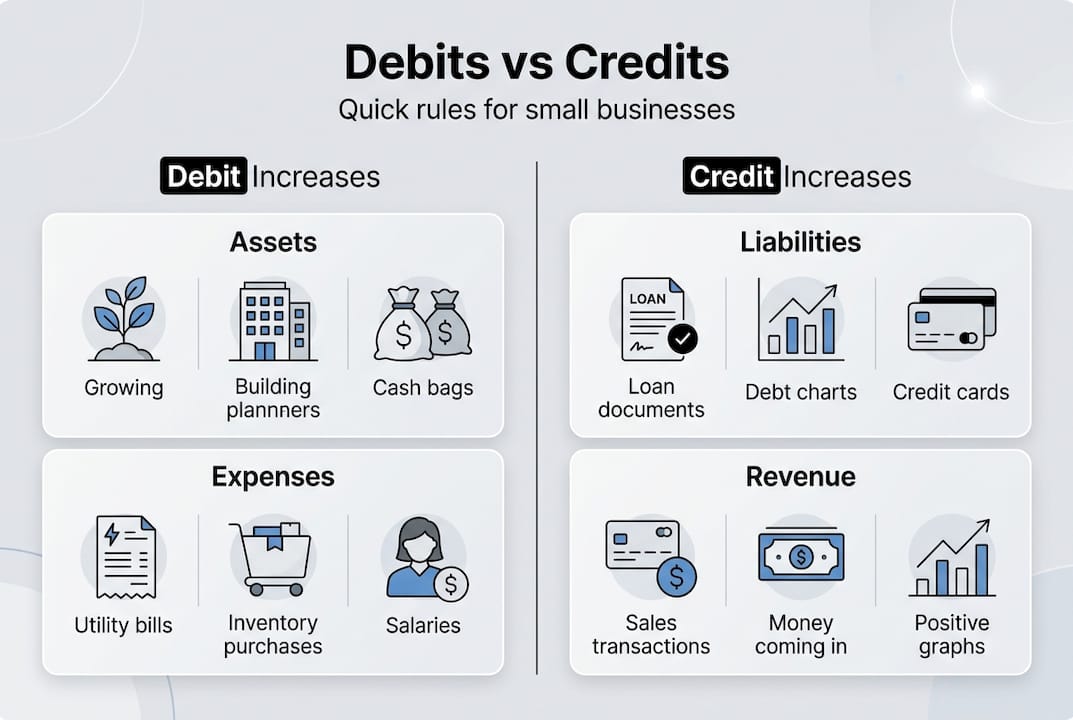

Debits and credits are simply entries in your accounting system. They’re not about gain or loss. They’re about tracking which accounts increase and which decrease when you record a transaction. Every business transaction affects at least two accounts, which is why we call it double-entry bookkeeping.

Here’s the fundamental rule: debits increase assets and expenses while decreasing liabilities, equity, and revenue. Credits do the opposite. They increase liabilities, equity, and revenue while decreasing assets and expenses. Debits and credits must always balance. If you debit one account for $500, you must credit another account for $500.

Think of it this way:

- Assets (cash, equipment, inventory) increase with debits

- Expenses (rent, supplies, utilities) increase with debits

- Liabilities (loans, accounts payable) increase with credits

- Equity (owner’s investment, retained earnings) increases with credits

- Revenue (sales, service income) increases with credits

This is completely different from your bank statement. When your bank debits your account, they’re taking money out. But in your books, a debit to your cash account means you’re adding money. The confusion happens because you’re looking at the transaction from different perspectives.

“The double-entry system ensures every transaction is recorded in at least two accounts, maintaining the fundamental accounting equation: Assets = Liabilities + Equity.”

Understanding bookkeeping for small business starts with mastering this core concept. Once you grasp how debits and credits work, everything else falls into place.

Why mastering debits and credits matters for small businesses

With the concepts defined, it’s crucial to see why getting debits and credits right really matters for your bottom line.

Bookkeeping errors aren’t just annoying. They’re expensive. Research shows that 44% of small businesses face bookkeeping errors leading to fines, with an average cost of $12,000 annually. That’s money you could invest in growth, equipment, or hiring.

For Kansas and Missouri business owners, accurate books are especially important. While standard GAAP rules apply to debits and credits in both states, local tax obligations require precise records. Kansas City’s 1% earnings tax, for example, demands accurate tracking of every transaction. Mistakes in your debit and credit entries can cascade into incorrect tax filings.

The real-world impact includes:

- Tax penalties and interest charges from incorrect filings

- Lost deductions because expenses weren’t properly categorized

- Cash flow problems from not knowing your true financial position

- Audit complications when records don’t balance

- Poor business decisions based on inaccurate financial reports

One of the most damaging mistakes is mixing personal and business transactions. When you use your business account for personal expenses without proper recording, your debits and credits get muddled. This makes it nearly impossible to understand your actual business performance.

Pro Tip: Set up separate bank accounts for business and personal use from day one. This simple step prevents 90% of debit and credit confusion.

Mastering debits and credits helps you maintain clean books for bookkeeping and tax compliance. It also gives you confidence during audits and helps you make informed decisions about pricing, hiring, and expansion. When you understand where your money is really going, you can spot opportunities and problems before they become critical.

The connection between bookkeeping accuracy and business success is direct. Accurate debits and credits mean accurate financial statements. Accurate financial statements mean better decisions and fewer costly surprises.

Debit and credit rules: Quick-reference table for business owners

Since the rules can feel abstract, visualizing how they work with each account type makes a big difference.

| Account Type | Debit Does This | Credit Does This | Normal Balance |

|---|---|---|---|

| Assets (Cash, Equipment, Inventory) | Increases | Decreases | Debit |

| Expenses (Rent, Supplies, Utilities) | Increases | Decreases | Debit |

| Liabilities (Loans, Accounts Payable) | Decreases | Increases | Credit |

| Equity (Owner’s Investment, Retained Earnings) | Decreases | Increases | Credit |

| Revenue (Sales, Service Income) | Decreases | Increases | Credit |

Many bookkeepers use the mnemonic DEALER to remember which accounts increase with debits: Dividends, Expenses, and Assets increase on Debit. Liabilities, Equity, and Revenue increase on Credit.

Let’s look at a practical example. When you make a cash sale, your Cash account (an asset) increases. Assets increase with debits, so you debit Cash. Your Sales account (revenue) also increases. Revenue increases with credits, so you credit Sales. The transaction balances.

Another helpful pattern: accounts that normally have a debit balance (assets and expenses) increase with debits and decrease with credits. Accounts that normally have a credit balance (liabilities, equity, and revenue) increase with credits and decrease with debits.

Pro Tip: Before recording any transaction, ask yourself two questions. First, which accounts does this affect? Second, does each account increase or decrease? Once you answer those questions, the debit and credit entries become obvious.

Keeping proper documentation in bookkeeping means recording every transaction with the correct debit and credit entries. This table serves as your quick reference whenever you’re unsure which side an entry belongs on.

Common scenarios: How debits and credits work in real-life transactions

Now, let’s bring these rules to life by seeing how debits and credits show up in actual business transactions you might encounter.

Example 1: Cash Sale

You sell $1,000 worth of products for cash. Here’s how you record it:

| Account | Debit | Credit |

|---|---|---|

| Cash | $1,000 | |

| Sales Revenue | $1,000 |

Cash (an asset) increases, so you debit it. Sales Revenue increases, so you credit it. The cash sale requires debiting Cash and crediting Revenue.

Example 2: Equipment Purchase on Credit

You buy $5,000 of equipment and agree to pay the vendor in 30 days:

| Account | Debit | Credit |

|---|---|---|

| Equipment | $5,000 | |

| Accounts Payable | $5,000 |

Equipment (an asset) increases, so you debit it. Accounts Payable (a liability) increases, so you credit it. You haven’t paid cash yet, but you’ve recorded both the asset you gained and the obligation you created.

Example 3: Sale on Account

You provide $2,500 in services and send an invoice:

| Account | Debit | Credit |

|---|---|---|

| Accounts Receivable | $2,500 | |

| Service Revenue | $2,500 |

Accounts Receivable (an asset) increases because the customer owes you money. Service Revenue increases because you’ve earned it, even though you haven’t collected cash yet.

Example 4: Contra-Asset Account

Depreciation is trickier. When you record $500 of depreciation on equipment:

| Account | Debit | Credit |

|---|---|---|

| Depreciation Expense | $500 | |

| Accumulated Depreciation | $500 |

Depreciation Expense increases (debit). Accumulated Depreciation is a contra-asset account that reduces the value of your equipment. It increases with a credit, which seems backward until you remember it’s reducing your total assets.

These examples show the patterns you’ll use repeatedly. Every transaction follows the same logic. Identify the accounts affected, determine whether each increases or decreases, then apply the debit and credit rules. Regular bookkeeping review examples help reinforce these patterns until they become second nature.

Pitfalls and errors: How to avoid bookkeeping mistakes with debits and credits

As you start using debits and credits, it’s critical to know where small businesses most often go wrong and how you can build habits that keep your books accurate.

The most common errors include:

- Reversing debits and credits: Recording a debit as a credit or vice versa doubles the error because both accounts are wrong

- Duplicate entries: Recording the same transaction twice, throwing off your balances

- Omitted entries: Forgetting to record a transaction entirely

- Misclassifying accounts: Putting an expense in the wrong category or confusing assets with expenses

- Confusing banking terms with bookkeeping terms: Mixing up debits and credits with banking definitions leads to backward entries

The banking confusion is particularly problematic. When your bank statement shows a debit, you might think you should debit your cash account. But if that bank debit represents money leaving your account, you should actually credit cash (decreasing an asset). This single misunderstanding causes countless errors.

Pro Tip: Reconcile your bank accounts monthly. This process catches debit and credit errors before they compound. When your books don’t match your bank statement, you know something’s wrong.

Accounting software helps tremendously. Programs like QuickBooks Online automatically create balanced entries for common transactions. When you record a sale, the software debits Cash and credits Revenue without you having to think about it. But you still need to understand the underlying logic to catch errors and handle unusual transactions.

Consider this insight:

“Research shows that 44% of small businesses face bookkeeping errors leading to fines, with an average cost of $12,000 per year. Many of these errors stem from fundamental misunderstandings of debits and credits.”

Outsourcing to a professional bookkeeper can cut your error rate dramatically. Experts who work with debits and credits daily spot mistakes you might miss. They also stay current on tax law changes and local reporting requirements. For many Kansas and Missouri small businesses, the cost of professional help is far less than the cost of errors.

If you’ve made mistakes, don’t panic. Most errors can be corrected with adjusting entries. The key is finding them quickly through regular reviews. Learning how to fix bookkeeping mistakes in QuickBooks can save you hours of frustration and prevent small errors from becoming big problems.

Taking control: Best practices for accurate bookkeeping in Kansas and Missouri

With the potential pitfalls in mind, here are the most effective, proven ways for Kansas and Missouri small business owners to keep debits and credits under control and protect their business.

-

Separate personal and business finances completely. Open a dedicated business bank account and credit card. Never mix personal transactions with business ones. This single step eliminates the majority of debit and credit confusion.

-

Reconcile your books monthly. Compare your accounting records to your bank statements every month. When they don’t match, investigate immediately. Monthly reconciliation catches errors while they’re still fresh and easy to fix.

-

Use accounting software designed for small businesses. QuickBooks Online, Xero, or FreshBooks automate many debit and credit entries. They also provide reports that help you spot unusual patterns or mistakes.

-

Review your financial statements regularly. Look at your profit and loss statement and balance sheet monthly. If something looks off, dig deeper. Trust your instincts.

-

Document every transaction. Keep receipts, invoices, and bank statements organized. Good documentation in bookkeeping makes it easier to verify your debit and credit entries later.

-

Stay current on local tax obligations. Kansas City’s earnings tax and other local requirements demand accurate books. Set reminders for filing deadlines and keep your records audit ready.

-

Consult a professional when needed. If your books are getting complex or you’re spending too much time on bookkeeping, get help. Outsourcing bookkeeping cuts errors by 50% and reduces audit risk by 80%.

Pro Tip: Schedule a specific time each week for bookkeeping. Consistency prevents the backlog that leads to rushed, error-prone entries. Even 30 minutes weekly is better than trying to catch up quarterly.

For Kansas City area businesses, understanding why bookkeeping matters in Kansas City goes beyond just debits and credits. It’s about maintaining compliance with local tax requirements, building a foundation for growth, and having confidence in your financial decisions.

Accurate debits and credits give you a clear picture of your business health. You’ll know exactly how much cash you have, what you owe, and whether you’re profitable. This clarity reduces stress and helps you plan for the future with confidence.

Get bookkeeping support: Take the next step for your business

If you’re ready for confident, compliant books and want expert help, here’s how to get support tailored for Kansas and Missouri small businesses.

Understanding debits and credits is essential, but applying them correctly month after month takes time and attention. Many small business owners find that outsourcing their bookkeeping frees them to focus on what they do best while ensuring their financial records stay accurate.

Professional bookkeeping support means your debits and credits are always correct, your books are reconciled monthly, and you’re ready for tax season without the last-minute scramble. You’ll have accurate profit and loss statements, clean balance sheets, and the peace of mind that comes from knowing your financial foundation is solid.

Whether you need help catching up on backlogged transactions, preparing for an audit, or simply want to hand off the monthly bookkeeping tasks, expert support is available. Kansas City area businesses benefit from working with professionals who understand both the technical requirements and the local tax landscape.

Ready to take control of your books? Schedule a free bookkeeping consult to discuss your specific needs and learn how professional support can help your business thrive.

Frequently asked questions

Do debits always mean money coming in and credits mean money going out?

No, debits and credits in bookkeeping are not the same as banking debits and credits. In accounting, they simply track which accounts increase or decrease based on standard rules.

Are there special bookkeeping rules for Kansas or Missouri?

No, standard GAAP rules apply to debits and credits in both states. However, accurate books are essential for meeting local tax filing requirements like Kansas City’s earnings tax.

What’s the easiest way to avoid debit and credit mistakes?

Reconcile monthly and use software like QuickBooks to automate entries and catch errors early. Consider consulting a bookkeeping professional for complex situations.

What happens if debits and credits don’t balance?

Your books will be out of balance, which produces incorrect financial reports and can lead to tax filing errors. Every transaction requires equal total debits and credits to maintain the accounting equation.

How often should I review my debit and credit entries?

Review your books at least monthly when you reconcile your bank accounts. Weekly reviews are even better for catching errors quickly and maintaining accurate records throughout the year.